Network Coopetition: An Empirical Analysis with Multiple Case Approach

|

|

|

- Deniz Renda

- 8 yıl önce

- İzleme sayısı:

Transkript

1 Network Coopetition: An Empirical Analysis with Multiple Case Approach By Duygu Aladag Dissertation Presented for the Degree of MSc in INTERNATIONAL BUSINESS and EMERGING MARKETS 2012/2013

2 ÖZET Ortaklaşa rekabet (coopetition), rakip firmaların stratejik amaçları doğrultusunda işbirliği içerisinde olmaları durumudur. Bu stratejik ilişki, konseptin ortaya atılmasından çok daha önce var olmasına rağmen, küresel rekabetin yüksek olduğu günümüzde ayrı bir önem kazanmıştır. Yükselen küresel rekabet, stabil olmayan ekonomik ve çevresel koşullar, kısıtlı kaynaklar ve yüksek maliyetleri göz önünde bulunduran rakip firmalar; ortaklaşa rekabet ile kaynak ve kapasitelerini bir araya getirerek üretim ve inovasyonda maliyet ve riskleri paylaşmaktadırlar. İş dünyasında ve akademik çevrelerce gösterilen ilgiye rağmen ortaklaşa rekabet konsepti halen yeterince araştırılmamış ve tüm yönleriyle keşfedilmemiştir. Konseptin karakteristik özellikleri ve kapsadığı alanlar açısından farklı görüşler mevcut olması nedeniyle; herkes tarafından kabul edilmiş kesin bir tanımı dahi mevcut değildir. Bu çalışma, ortaklaşa rekabet literatürüne teorik ve ampirik açıdan katkı sağlamayı amaçlamaktadır. Teorik katkı olarak; ortaklaşa rekabet üzerine var olan literatür analizi ardından konseptin doğası ve avantajları üzerine teorik bir çerçeve oluşturulmuş; ve konsept için bir tanım yapılmıştır. Bu çalışmanın ampirik katkısı ise; ortaklaşa rekabetin; özellikle ağ ortaklaşa rekabetinin (network coopetition) doğasının ve avantajlarının sergilendiği iki adet vaka analizi olmuştur. İlk vaka analizinde ortaklaşa rekabet ağlarının inovasyon yaratımına katkısının örneği olan EUREKA projeleri ele alınmıştır. Bu vaka analizi ayni zamanda KOBİ lerin ve büyük işletmelerin ortaklaşa rekabete olan yaklaşımlarındaki farklılıkları da gözlemleme imkânı sunmuştur. İkinci vaka ise, ortaklaşa rekabetin önemli bir karakteristik olduğu küresel havayolu endüstrisini mercek altına almıştır. Bu vakada Türk Hava Yolları nın Star Alliance a katilim süreci ve Alliance a katilimin THY ye olan katkılarının incelenmesi, ortaklaşa rekabetin doğası ve avantajlarına dair zengin bir kaynak olmuştur. Ortaklaşa rekabetin doğası ve avantajları hakkındaki bulguların yanı sıra, bu çalışmanın en önemli katkılarından biri ağ ortaklaşa rekabetinde düzenleyici/koordine edici bir kuruluşun öneminin vurgulanması olmuştur. Önceki akademik çalışmalarda değinilmeyen bu hususta, EUREKA ve Star Alliance önemli örnekler olmuşlardır.

3 ABSTRACT Coopetition concept refers to a strategic relationship among competitor firms, where they compete and cooperate simultaneously. Coopetition promises significant advantages for firms in the era of intensive global competition. Although coopetitive relationships existed long before the term was coined, the conditions of contemporary business world make increasing number of firms adopt coopetitive strategies in order to share costs, risks, or lead innovations, by collectively deploying their resource and capabilities with competitors. In spite of the increased interest on the topic, coopetition remains as an under-researched area. It even does not have a commonly accepted definition, regarding the variety of approaches on its defining characteristics and borders. This study provides both theoretical and empirical contributions to the concept of coopetition. Theoretically, after the analysis of the literature on coopetition, it provides a definition of coopetition, as a strategic relationship where firms from the same industry compete and cooperate simultaneously within a dynamic structure, in order to benefit from the synergies and efficiencies created through the common deployment of resource and capabilities in various areas and stages of their businesses. Furthermore, it provides a framework on nature and advantages of coopetition. Empirically, two case studies contribute to the understanding on the nature and advantages of coopetition, specifically on coopetitive networks. The first case study is about EUREKA projects, enabling us observing network coopetition in terms of R&D and innovation creation, which is considered to be of the most substantial areas to coopete. Moreover, the case provides a comparison between SMEs and large companies in terms of their approach towards coopetition. The second case puts global airline industry under scope, in which network coopetition is an industry-defining characteristic. The case specifically analyses the process of Turkish Airlines to join Star Alliance, and the effects of the alliance membership to the company, which became a rich resource to exemplify the advantages and setbacks of network coopetition in airline industry. Additional to the insights on nature and advantages of coopetition, one of the most remarkable findings of this study have been demonstrating the key role of the coordinating organisations on

4 network coopetition (EUREKA in first case study and Star Alliance at the second), which is an issue have not addressed by previous research.

5 ACKNOWLEDGEMENTS My sincerest thanks To my supervisor Dr. Tanja Kontinen, for your support, motivation, and guidance throughout writing my dissertation. To all interviewees, for your time and invaluable information you generously provided. To European Union s Jean Monnet Scholarship Programme, for providing me the opportunity of having an MSc degree from one of the world s most prestigious universities. To my dearest friends, you became my second family in Edinburgh and made this year an unforgettable journey. To Martin, for making the world smaller, for sharing this life changing experience with me, and for all your love and support. Finally, the biggest thanks to my family, Nedime and Mehmet. You taught me the two greatest things in this life: love, and constantly fighting for my dreams. I am proud of being your daughter.

6 Table of Contents 1. INTRODUCTION LITERATURE REVIEW Competition, Collaboration and Coopetition Components of coopetition: Competition and Collaboration Nature of coopetition: Paradoxical, Multidimensional and Multifaceted Increased interest on topic Lack of definition Defining Coopetition Who actually coopetes? The timing of competition and cooperation Are strategic alliance and coopetition same things? Definition of Coopetition Theoretical Background of Coopetition Game Theory Resource Based View Knowledge Based View Network Economy Types of coopetition Network Coopetition Advantages of coopetition Cost Related Advantages Market Standardization and Lobbying Advantages on Learning and Innovation Setbacks about Coopetition: Opportunism Threat and Trust Issue The importance of the coordinating organisation in Network Coopetition Comparing SMEs and large companies in terms of coopetition METHODOLOGY Case Study Design Interviews Case One: EUREKA Case Two: Turkish Airlines The analysis of interviews ETHICAL CONSIDERATIONS... 4

7 4. CASE 1: EUREKA Network Coopetition in Eureka Eurostars Programme: SMEs in Network Coopetition Eureka Clusters Analysis of the Programmes Advantages of Eurostars and the Clusters Differences between SMEs and large companies CASE2: AIRLINE NETWORK COOPETITION - TURKISH AIRLINES IN STAR ALLIANCE Global Airline Industry: A Snapshot Alliances: Major Actors of the Industry The Factors Shifting Industry towards Alliances Star Alliance Advantages of Star Alliance Joining Star Alliance: How to Become a Member Turkish Airlines About the Company Turkish Airlines and Star Alliance Deciding to Join Star Alliance: Decision And Integration Processes Star Alliance-Turkish Airlines Relationships Benefits for Turkish Airlines: Prestige and Increased Brand Awareness Disadvantages of Star Alliance Findings on Nature of Coopetition n Airline Industry Do All Participants Benefit Equally? Increased Level of Competition Future of Coopetition in Airline Industry Conclusion Cross Case Analysis Similarities On Advantages of Coopetition Differences CONCLUSION LIMITATIONS AND DIRECTIONS FOR FUTURE RESEARCH REFERENCES... 48

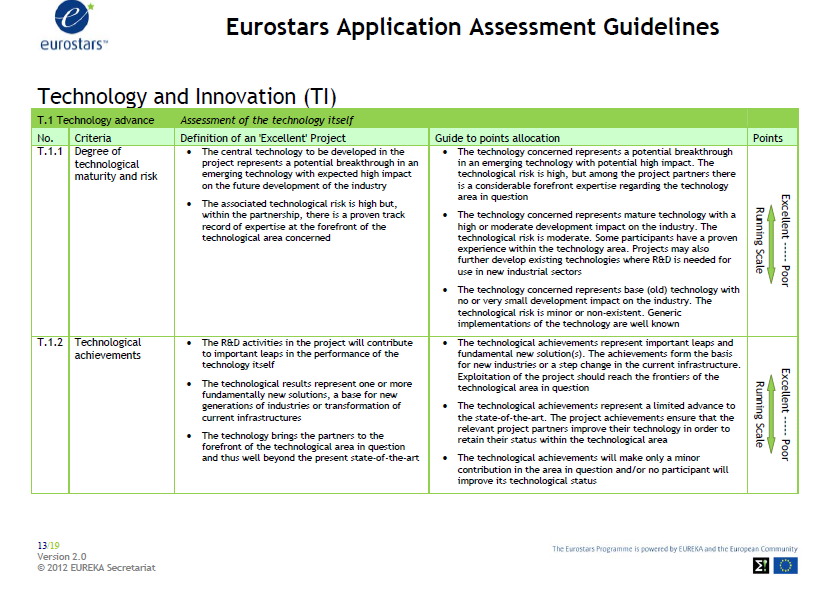

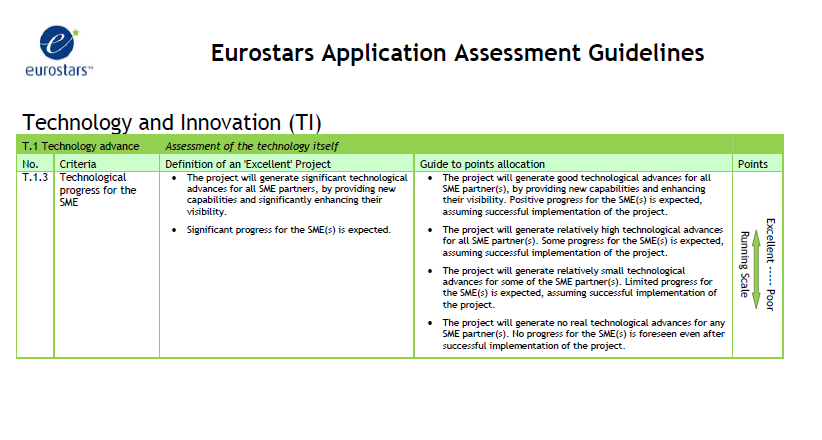

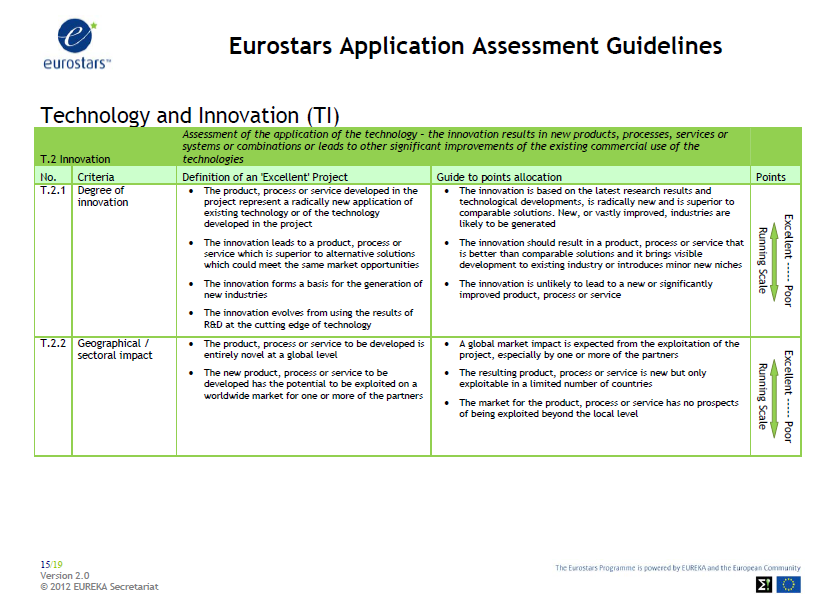

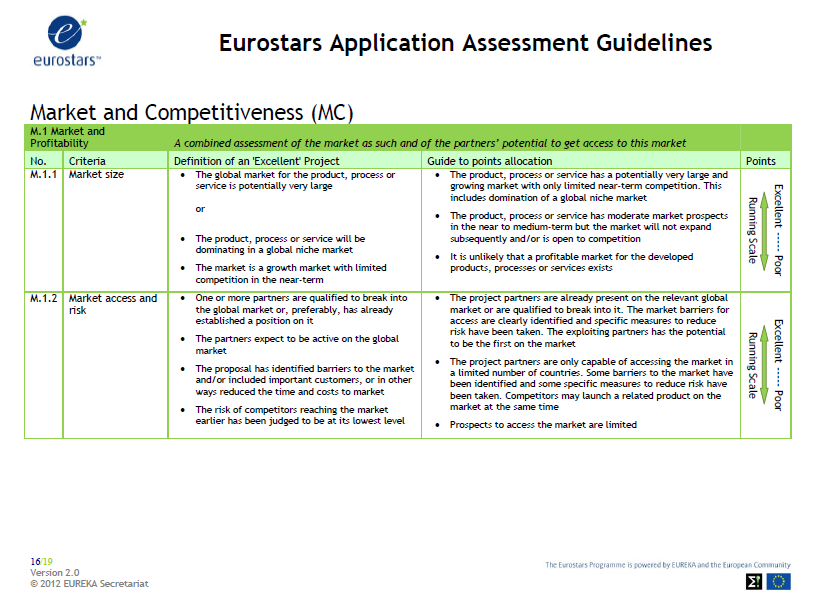

8 APPENDIX 1- TRANSCRIPTION: Interview With Serhat Sari- Turkish Airlines Scotland General Manager ORIGINAL INTERVIEW-IN TURKISH TRANSLATION to ENGLISH APPENDIX 2- TRANSCRIPTION: Interview with Fatma Basaran Çiçek, Turkish Airlines Edinburgh-Regional Commercial Manager- Turkish Airlines Edinburgh Directorate ORIGINAL INTERVIEW-IN TURKISH TRANSLATION to ENGLISH APENDIX 3- TRANSCRIPTION: Interview with Onur Alpan-Turkish Airlines, Internatonal Relations and Agreements Manager; and Banu Ekerim- Turkish Airlines International Alliances Specialist ORIGINAL INTERVIEW: IN TURKISH TRANSLATION to ENGLISH APPENDIX 4- TRANSCRIPTION: Interview with Marej Jazak, Impact & Portfolio Analyst ar EUREKA Secretariat and Piotr Pogorzelski, officer at EUREKA Secretariat, and Lecturer at European Institute of Public Administration APPENDIX 5- TRANSCRIPTION: Interview With Emre Yurttagul, EUREKA Turkey- International Project Coordinator ORIGINAL INTERVIEW: IN TURKISH TRANSLATION to ENGLISH APPENDIX 7- EUREKA Historcal Evolution of EUREKA EUREKA MEMBER COUNTRIES EUREKA UMBRELLAS SAMPLE CONFIDENTIAL AGREEMENT EUROSTARS CONSORTIUM SKELETON A Sample Project Management Structure, from Celtic Plus Eurostars Programme Funding excellence in innovation Eurostars Application Assessment Guidelines,

9 LIST OF TABLES Table 1: Matrix of strategic alliance and coopetition Table 2: Theories and views related coopetition Table 3: Types of coopetition Table 4: Table of Interviews... 1 Table 5: Thematic Approach on Interviews... 3 Table 6: Ethical Issues and the reflections of this study... 4 Table 7: SME definition by the European Union... 7 Table 8: EUREKA Clusters Table 9: Members of the three airline alliances Table 10: Basic facts on Star Alliance Table 11:Ranking of European airlines... 37

10 TABLE OF FIGURES Figure 1: Positioning coopetition between pure competition and pure collaboration... 4 Figure 2: Porter s 5 forces and Nalebuff and Brandenburger s 6th force, complementors Figure 3: Coopetitive networks competing each other Figure 4: Advantages of coopetition Figure 5: Knowledge Creation Cycle on Coopetition, adapted from Ritala et al. (2009) Figure 6: Triangulation of the Research Figure 7:Eureka Projects as Dyadic and Network Coopetition Formations... 6 Figure 8: Distribution of Organizations Participating in EUREKA Projects... 7 Figure 9: Participants in Eurostars Projects... 7 Figure 10: Types of Eurostars Consortiums... 8 Figure 11: Eurostars Project Approval Process... 9 Figure 12:Eureka Clusters and forms of coopetition Figure 13:The process of cluster projects Figure 14: Advantages of coopetition mentioned at the literature review Figure 15: Consortium Requirements for Successful Coopetition Figure 16: EUREKA Label Figure 17:Direction of the Case Figure 18: Market Value of Global Airline Industry Figure 19: Competition in Global Airline Industry Figure 20: A snapshot on the market share of alliances Figure 21:Advantages of Coopetition in Airline Industry Figure 22 Global Network of Star Alliance Figure 23: Membership Process for Star Alliance Figure 24: Turkish Airlines Organisational Structure Figure 25: Facts and Figures about Turkish Airlines Figure 26: Increased competition amongst competitors Figure 27:Advantages of coopetition in both cases... 42

11 1. INTRODUCTION Coopetition is a strategic relationship, where competitors are involved in cooperation, in order to realize their specific goals (Ritala and Wegmann, 2011). Although the cooperative relationships of competitors existed before the term was coined, the concept gained popularity after Brandenburger and Nalebuff s famous book Coopetition (1996). Coopetition enables firms to combine the advantages of competitive and cooperative strategies. However, coopetition is a dynamic and paradoxical nature (Guardo and Galvagno, 2007), regarding the contradicting natures of cooperation and competition. This is the main factor making coopetition different from any other kind of collaborative relationship (Ritala and Hurmelinna-Laukkanen, 2009), (Bengtsson on and Kock, 2000). In the era of global competition, where interdependence, constant change, and instability are defining features of the contemporary business world; increasing number of firms from various industries adopt coopetitive strategies, in order to share costs and risks, or lead innovations by deploying their resources and capabilities to complement each other. In spite of the increased interest on coopetition from firms as a strategic tool, and from academic studies as a research subject, there is still no consensus on its definition. Indeed, the lack of a commonly accepted definition prevents building a strong conceptual and theoretical framework (Galvagno and Garraffo, 2007). In spite of many studies claiming the importance of the subject as a strategic tool, literature on coopetition still carries many gaps. This study provides theoretical and empirical contributions on coopetition. First, after a discussion of the contested features leading the conflict on definition of the concept, it provides a definition in coopetition. Moreover, it analyses the previous literature in order to provide a framework on the nature and advantages of coopetition. Indeed, that part provides a basis for the empirical contributions of the study, as it is not possible to carry an exploratory inquiry towards a concept without clearly defining what it actually is. 1

, regarding the contradicting natures of cooperation and competition.")

12 Following the theoretical part, the empirical part of the study analyses coopetition in network level, in order to gain more insights about the nature of coopetition within a more dynamic environment. With that motivation, two case studies were conducted, by searching answers for the following questions: 1. How is the nature of coopetition and what are the advantages of coopetitive strategy? 2. What is the role and importance of a coordinating organisation in network coopetition? 3. What are differences between SMEs and large companies in terms of their approach towards coopetition? The first case study on EUREKA projects enables us observing network coopetition in terms of R&D and innovation projects, which is considered to be one of the most substantial areas to coopete. Moreover, the case provides a comparison between SMEs and large companies, and exposes the importance of EUREKA as a coordinating organisation within network coopetition. The second case analyses network coopetition within global airline industry, where coopetition is an industry-defining characteristic. The case tackles the process of Turkish Airlines to join Star Alliance, and the contributions of the alliance to the company; which demonstrated the advantages and setbacks of coopetition in airline industry. The case also demonstrates the key role of Star Alliance as a coordinating organisation of the biggest coopetitive network of the industry. 2

13 2. LITERATURE REVIEW Coopetition is, with its very basic description, competing and collaborating simultaneously. (Bengtsson and Kock, 2000), (Levy et al., 2003). Within a coopetitive relationship, firms closely collaborate and intensively compete at the same time (Breznitz, 2007), in order to realize their specific goals (Ritala and Wegmann, 2011). Firms involved in a coopetitive relationship collaborate to create value, and compete to get the biggest share of the value created (Nalebuff, and Brandenburger, 1996). Coopetition concept gained popularity after Nalebuff and Brandenburger (1996) carried the concept into a more popular stage with their famous book Coopetition. Nalebuff and Brandenburger (1996) and many other studies (Dagnino and Padula, 2002), (Luo, 2007) claimed that the word coopetition was first used by Raymond Noorda, CEO of Novell Company, describing Novell s business strategy. However, the word was coined far before than Noorda did. In 1913, P.T Cherington put the words of an oyster manufacturer Kirk P. Pickett in his book, who used the word coopetition for the first time in the literature, while describing the relationship between the oyster dealers: You are only one of several dealers selling our oysters in your city. But you are not in competition with one another. You are co-operating with one another to develop more business for each of you. You are in co-opetition, not in competition (Cherington, 1913). Indeed, coopetitive relationships existed before the term gained popularity. Hamel et al. (1989), for instance, claimed that collaborating with competitors would be a great source of competitive advantage. However, coopetitive formations became increasingly popular during the last two decades. Globalisation of the business world made all economic actors interdependent on each other, even competitors (Luo, 2004). Competitors face similar challenges in the market (Chen, 1996), where managing those challenges solely with their own resources and capabilities would not be possible; even if it were, that might not be the most efficient way. The resource-asymmetries of competitors stimulate coopetition, where coopetitors can deploy their resources to complete each other effectively. As Nalebuff and Brandenburger (1996) remark, coopetition is an open-minded position that also 3

carried the concept into a more popular stage with their famous book Coopetition.")

14 embraces complementary elements of competitors. In a world where firms face serious challenges of global competition, more and more firms realise the potential of advantages from cooperating with competitors, regarding their similarities in terms of resource, capability and challenges Elmuti et al., 2012), (Liedtka, 1996) Competition, Collaboration and Coopetition Coopetition is somewhere at the continuum between the pure competition and pure collaboration, (Galvagno and Garraffo, 2007), (Eriksson, 2008), which promises greater benefits than discrete competitive or collaborative strategies (Le Roy and Guillotreau, 2010), by providing firms the advantages of both competition and collaboration. (Yami et al., 2010). The involvement of competitive characteristics into a collaborative relationship makes collaboration of competitors much different than collaboration of non-competitors (Ritala and Hurmelinna-Laukkanen, 2009), (Bengsston and Kock, 2000). For this reason, it is essential to avoid approaching coopetition as a simple collaborative relationship. Indeed, coopetition is perceived as a new kind of interdependence for value creation (Dagnino and Padula, 2002), or a new type of strategic relationship (Akdogan and Cingoz, 2012), (Bouncken and Fredrich, 2012). Figure 1: Positioning coopetition between pure competition and pure collaboration COOPETITION PURE COMPETITION PURE COOPERATION Resource: Galvagno and Garraffo, Components of coopetition: Competition and Collaboration In order to obtain a better understanding towards coopetition, it is important to bring together the definitions and main characteristics of the two components of the concept Competition 4

, (Liedtka, 19")

15 Competition: The activity of condition of striving to gain or win something by defeating or establishing superiority over others. -Oxford Dictionary of English As its definition clearly demonstrates, in a competitive relationship, involving parts endeavour to defeat each other to obtain superiority over the rest. Rivalry occurs because one or more competitors either feels the pressure or sees the opportunity to improve position (Porter, 1980). The competitive way of value creation is a zerosum game, where one part s gain becomes the other part s loss. In competition strategy, the value creation takes place within the firm, whereas the interaction with other competitors take place in the distribution of the value created (Porter, 1980) Cooperation Cooperation: The action or process of working together to the same end. -Oxford Dictionary of English Following the rise of competition strategy, cooperation emerged as an alternative, regarding the interdependence of firms originated from their converging interests (Simoni and Caiazza, 2012). In a cooperative relationship, involving parts deploy their resources, capabilities, and efforts for reaching a common goal. It is a positivesum game in a formation of strategic interdependence (Dagnino and Padula, 2002). Cooperative perspective is based on the logic that firms can get superior position by developing common interests (Gulati 1998), (Abdallah and Wadhwa, 2009) Nature of coopetition: Paradoxical, Multidimensional and Multifaceted Being simultaneous competition and collaboration, coopetition possess different characteristics than cooperation of non-competitors. Regarding the contradicting natures of competition and collaboration, sleeping with the enemy (Coy, 2006) has a paradoxical nature (Guardo and Galvagno, 2007), (Schmlele and Sofka, 2007), (Bengtsson and Kock, 2000). The combination of those contradicting concepts make coopetition very dynamic and unstable, as it is shaped by constant action and reaction of the interdependent firms involved (Castaldo and Dagnino 2009). Regarding its nature summarized above, coopetition is a win-win game, however the results are changeable (Dagnino, 2009) and ambiguous (Dagnino and Padula, 2002), dependent on the actions of the involving parts. 5

16 Moreover, the number of the firms involved, the industry they operate in, which part of their business they coopete and and many internal/external factors make it impossible to generalize about whether competition or cooperation weights heavier in a coopetitive relationship. As Luo (2005) states, these contradicting elements are dynamic, the dominance of one on another constantly change regarding the changes in the external environment and the firm s needs. It can be competition or cooperation dominated, or balanced (Bengtsson and Kock, 2000). To conclude, coopetition is a multidimensional and multifaceted concept, carrying structural variability dependent on many factors and characteristics of the involving parts, which makes it difficult to provide generalizations about significant characteristics of the relationship, such as whether competition or collaboration weights heavier Increased interest on topic Increased and intensified global competition and extremely fast changing environment make increasing number of firms from various industries form coopetitive relationships, regardless of the degree of their rivalry. Markets do not consist of atomised and isolated actors anymore, but interactive systems like living organisms where actors continuously interact with each other to survive and prosper (Dagnino and Padula, 2002). Interfirm connections has become so crucial that, the competitive advantage of the firm gets dependent on its ability of building competitive and cooperative relationships better than anyone within the market (Guardo and Galvagno, 2007). In such conditions, it is not surprising that increasing number of firms choose coopetition as a strategic tool and that the interest towards coopetition as a research subject increases (Galvagno and Garaffo 2007), (Dagnino and Padula, 2002), (Lado et al., 1997), (Gnyawali and Madhavan, 2001) Lack of definition In spite of the increased interest and numerous academic studies on coopetition, there is still no consensus about its definition. The lack of a commonly accepted definition also prevents building strong conceptual and theoretical frameworks for coopetition, e.g. if there is no consensus about who is actually coopeting. As Galvagno and 6

.")

17 Garraffo (2007) states, the situation prevents coopetition to flourish as a distinctive research area, where many studies do not go further beyond than naming, claiming or evoking it (Dagnino and Padula, 2002). First and foremost, coopetition needs a generally accepted definition, and then a strong conceptual framework defining the borders, nature and issues related. Then this conceptual framework should be strengthened with in-depth case studies from various industries Defining Coopetition This section aims to provide a definition of coopetition, by discussing the most important dissidences on definition of coopetition: the actors involved in, the period it covers, and the misuse of strategic alliance as a synonym of coopetition Who actually coopetes? There are two main approaches towards the issue of what type of actors actually coopete. The first approach has its roots from Nalebuff and Brandenburger s book Coopetition (1996). Brandenburger and Nalebuff claim that, Porter s five forces model is insufficient and there should be a sixth type of actor within the model: complementors. Complementors are actors who complement one good or service by adding value for the common users. For instance, software and hardware products are complementors to each other; and Nalebuff and Brandenburger claim that not only competitors but also complementors coopete each other (figure 2). Following this approach, Afuah (2000) claims that stakeholders are also coopetitors. Bouncken and Fredrich (2012) also define coopetition as the relationship with varying degrees of competition and collaboration that is carried out horizontally between classic competitors and vertically between up and downstream partners that collaborate but also compete about their share of the pie. 7

18 Figure 2: Porter s 5 forces and Nalebuff and Brandenburger s 6th force, complementors. suppliers Complementors potential entrants industry competitors: rivalry among existing firms substitutes buyers Source: Nalebuff and Brandenburger 1996; Porter, 1980 The second approach, which is also adopted by this study, claims that coopetition is the simultaneous competition and collaboration, where only competitor firms involve in (Bengtsson and Kock, 2000). In other words, this approach accepts coopetition as the collaboration in the horizontal level. Integrating vertical collaborations into the domains of coopetition concept would mean taking suppliers, buyers, even stakeholders as a firm s competitors; which would lead approaching every type of relationship among these actors as coopetition, which in turns, would be a logical mistake contradicting the nature of the concept itself The timing of competition and cooperation Another important dissidence about coopetition is about when actors exactly compete and cooperate. There are three approaches about the issue: 1) Competition and cooperation should be simultaneously (Ritala et al, 2009), (Luo, 2007) 2) Firms compete in one period of time and cooperate in another ; (Chien and Peng, 2005) 3) Firms can compete and collaborate either simultaneously, or sequentially (Galvagno and Garraffo, 2007), (Ritala and Wegmann, 2011) 8

19 This study adopts the first approach, considering the fact that competitor firms do not surcease their rivalry just because of they are involving in a kind of cooperative formation in a specific area. Regarding the global business conjuncture and intensified multimarket rivalry, it would not be realistic to assume that firms follow a sequence of competition and collaboration Are strategic alliance and coopetition same things? Another confusion about coopetition is the misuse of strategic alliance and coopetition, as they were synonym concepts. If the borders of coopetition were kept such wide to cover suppliers, competitors and customers, it is even possible to argue that coopetition is no different from strategic alliances. Coopetition is a collaborative formation, taking place between competitors. A strategic alliance, on the other hand, is a formation where two or more companies are involved, in order to reach a common goal (Barney 2011), (Das 2000). The important point here is, a strategic alliance can take place among any actors: between competitors, or non-competitors. If a strategic alliance takes place among vertical actors, such as a strategic alliance between suppliers and producers, that has nothing to do with coopetition. However, if the strategic alliance takes place between competitors, then this strategic alliance is a coopetitive alliance, just as many studies focused on that type of coopetitive-alliances (Khanna et al 1998), (Dussauge et al., 2000), (Bengston and Kock, 2000),(Gnyawali and Park 2009), (Akdogan and Cingoz, 2012). Indeed, the majority of strategic alliances take place in the form of coopetition. In 1998, 15 years from today, Harbison and Pekar claimed that, over 50 percent of the strategic alliances take place between competitors. Regarding the increased competition and the contemporary conditions in the global economy, it would not be a wrong estimation to claim that this ratio should have even increased. 9

20 Table 1: Matrix of strategic alliance and coopetition Competitor+Competitor Non-competitor+Noncompetitor COOPETITION YES NO STRATEGIC ALLIANCE YES YES 2.6. Definition of Coopetition Regarding the discussion in the previous chapter, the study provides a clear definition of coopetition: Coopetition is a strategic relationship, where firms from the same industry compete and cooperate simultaneously within a dynamic structure, in order to benefit from the synergies and efficiencies created through the common deployment of resource and capabilities in various areas and stages of their businesses Theoretical Background of Coopetition The literature so far has associated coopetition with Game Theory, Knowledge Based View, Resource Based View, and Network Economy View. Considering all of these theories help to enlighten different aspects of the nature of coopetition (table 2), this study adopts a holistic approach in terms of theoretical background, rather than building concept based solely on one of the views introduced below Game Theory Game theory is the study of mathematical models of conflict and cooperation between intelligent rational decision makers (Myerson, 1991). Myerson s definition clearly illustrates how game theory fits to explain the nature of coopetition, as coopetition is a continuous interplay of competitors, who become interdependent on each other. Following Brandenburger and Nalebuff (1996), who rooted coopetition on game theory in their famous book Coopetition, various studies rooted their coopetition studies on game theory (Herzog 2010), (Devetag, 2009). From the perspective of game theory, coopetition is a variable-sum game, where firms 10

21 cooperate for value creation, and compete for getting the most from the value collectively created (Brandenburger and Nalebuff, 1995). Ritala and Hurmelinna- Laukkanen (2009) claim that firms involve in value creation via cooperation, and value appropriation in competition while coopeting Resource Based View Resource based view claims that sustainable competitive advantage of the firm can be achieved through retaining (Barney, 1991), manipulating and deploying (Sirmon et al., 2007) unique resources (Gnyawali and Park 2009). Resource based-view helps to explain the importance of sharing and deployment of resources among competitors within coopetitive formations. When a firm s own capabilities are solely not enough to manage all challenges and demands of the contemporary globalised competition, the access to and successful deployment of resources gained through coopetition might play vital role for forms to survive and prosper Knowledge Based View Knowledge based view, having its roots from the resource based view (Curado, 2006), approaches knowledge as the most valuable asset that a firms holds (Dunning, 2000), (Liebeskind, 1996). Over the last three centuries, the main source of wealth in market economies has switched from natural assets (notably land and relatively unskilled labour), through tangible created assets (notably buildings, machinery and equipment, and finance), to intangible created assets (notably knowledge and information of all kinds) which may be embodied in human beings, in organizations, or in physical assets Dunning (2000). Knowledge-based view of the firm elucidates the importance of coopetition in terms of strengthening the knowledge base through inter-organisational learning, and leading innovations via coopeting, as will be addressed in more details on knowledge, learning and innovation related advantages of coopetition Network Economy Network theory is about the importance of the ties that firms create, focusing on the importance of using network relationships to access and exploit external resources, 11

22 and using them for the firm s own benefits. Tomski (2011) claims that, firms are not isolated forms like atoms; network is the concept best describing the economy of 21 st century. The existence of a network is an extremely important phenomenon because just on account of its business units to have access to the resources of another participant. In terms of coopetition, network approach provides understanding on the importance of getting access to resources outside the firm, and what types of relations serve best to the purpose Powell et al (1996). Table 2: Theories and views related coopetition Theory GAME THEORY Relation with coopetition Coopetition is a variable-sum game, where firms cooperate to create value and compete to get the most of the value created. RESOURCE BASED VIEW KNOWLEDGE BASED VIEW NETWORK ECONOMY Firms aim to obtain and deploy valuable resources to gain competitive advantage, via cooperating with their competitors Knowledge is the most valuable asset of the firm. Competitors can increase their knowledge-based capabilities via sharing of knowledge, and creating new knowledge via coopetition. Firms can access to the resources of competitors within via a coopetitive network. 12

23 2.8. Types of coopetition There are many studies providing different classifications for coopetition, in terms of the number of the parties involved, the level of integration, and the number of areas that coopetition takes place (Bengtsson and Kock, 2000), (Gnyawali and Madhavan, 2001), (Dagnino, 2009). In this study, inspired by (Dagnino and Padula,2002), coopetition will simply be grouped in two levels: coopetition in dyadic level; which is coopetition arising among two firms; and coopetition in network level, which occurs with involvement of more than two firms (table 3). Table 3: Types of coopetition Number of firms involved Two More than two Type of coopetition Dyadic coopetition Network coopetition This study focuses on network coopetition, aiming to gain substantial insights on the nature of coopetition, regarding the dynamic nature where multiple actors involved. Companies have created networks of alliances in order to command competitive advantages that individual companies of traditional two-company alliances cannot (Gomes-Casseres, 2000) Network Coopetition Network coopetition is a kind of collaborative formation, where more than two competitor firms involved, aiming to achieve superior advantages by sharing and collective deployment of resource and capabilities. As in any form of coopetition, firms involved in network coopetition collectively create value via cooperation, and compete to get the biggest share from the value created. A company in a coopetitive network has to keep its eyes on both competences which create value and capture it at the same time (Abdallah and Wadhwa, 2009). Compared to dyadic coopetition, network coopetition provides access to larger level of resources from many firms, especially in terms of knowledge and learning (Lado et al., 1997), (Bernal et al., 2002); getting informed about the developments of the 13

24 industry, and access to higher level of information about their rivals within the network (Gulati et al., 2000), (Gnyawali and Madhavan, 2000). Gulati (1999) claims that, the relationships built within networks catalyse further partnerships. In other words, the more network resources the firm accesses, the more coopetitive relationship opportunities rise. Accordingly, the increased network coopetition might turn some industries consist of coopetitive networks competing each other (Garaffo, 2002), (Gomes-Casseres, 1994), (Todeva and Knoke, 2005), as illustrated in figure 3. Figure 3: Coopetitive networks competing each other Coopetition coopetit ive network coopeitive network coopetitiv e network Coopetiti Coopetition 14

25 2.9. Advantages of coopetition Being the simultaneous combination of competition and cooperation, coopetition enables firms to reap advantages of both competitive and cooperative strategies (Yami et al., 2010). The ultimate result of all these advantages is the increase in firms competitive advantage (Hamel et al., 1989). Advantages of coopetition touched by existing literature can be categorized under three groups, as cost related, market related, and learning & innovation related advantages (figure 4). Figure 4: Advantages of coopetition COST RELATED bargaining power market standardization, lobbying economies of scale advantages of coopetition cost sharing risk sharing knowledge share increased innovation and learning 15

26 Cost Related Advantages As will be exemplified by case studies on section 4 and 5, competitors obtain cost related advantages from coopetitive strategy, such as cost sharing, economies of scope and scale on manufacturing or new product development (Luo 2005). This is a significant advantage especially for SME s, who has insufficient financial resources for purchasing of expensive machinery or equipment. (Gomes-Casseres, 1997) Market Standardization and Lobbying Regardless of the industry origin, coopetitive networks provide firms to involve in lobbying activities, in order to raise a common voice on shaping industry standards, or position against the regulations or interventions set by governments or any related organisations, in order to maximize the overall benefits of the industry (Luo, 2005), (Abdallah and Wadhwa, 2009). Another aspect of market standardization particularly takes place in terms of innovation. As Tether (2002) claims that, firms are likely to involve in coopetition for higher level innovations, in order to create pioneering technologies for that particular industry. Once an industry-shaping innovation is created, firms have chance to involve in market standardization process. Nonetheless, it is also a possible case that two or more coopeting networks to introduce such innovations, and then compete against each other to make their innovation the market shaping one. The competition takes place in the form of endeavour to attract more businesses to adopt their product and services aligned with the network s innovation (Gomes-Casseres, 1994) Advantages on Learning and Innovation As knowledge based view emphasises, knowledge base of a firm is one of the most important resources to obtain and endure competitive advantage. Why then firms consider sharing knowledge with a competitor in a coopetitive relationship? The answer is, coopetition fosters collective intelligence through knowledge and information sharing (Osarenkhoe, 2010). Knowledge sharing among competitors would lead synergies (Levy et al., 2003), (Akdogan and Cingoz, 2012), (Luo, 2005); which is claimed to be greater than the synergies generated through knowledgesharing cooperative agreements among non-competitors (Ritala and Hurmelinna- 16

27 Laukkanen, 2009). The reason lying behind that synergy is the similar resources and perspectives the competing firms have (Dussauge et al., 2000), which would complement each other to create valuable knowledge and inter-partner learning (Hamel, 1991). While coopeting, competitors gain access to the valuable resources, which would stimulate innovations that firms could not achieve alone; or could only be achieved within a considerably longer period (Von Hippel, 1987). Coopetition enables access to not only technological knowledge, but to the skills and other capabilities of the partners (Gnyawali and Park 2009), (Hamel et al., 1989), such as management and marketing skills (Bigliardi et al., 2011). Access to the knowledge of competitors foster inter-partner learning either it is a dyadic (Dussage et al. 1999), or network (Johnsen and Johnsen, 1999) coopetitive relationship (Bengtsson and Kock, 2000). Ritala et al. (2009) provides a process model of innovation and knowledge creation of coopetition, which can be summarised as follows: Once the knowledge is shared with the coopetitor, the new knowledge is combined with the firm s tacit knowledge. The more knowledge obtained and created, the more coopetitive manoeuvres take place (figure 5). Figure 5: Knowledge Creation Cycle on Coopetition, adapted from Ritala et al. (2009) knowledge shared with competitor new knowledge created internalize with tacit knowledge collective intelligence 17

28 In addition to knowledge sharing, coopetition boosts innovation by sharing costs, capabilities and risks related to innovation process (Schmlele and Sofka, 2007), (Veryzer, 1998), (Watanabe et al., 2009), (Khanna etal.,1998), (Afuah, 2000). Coopetition stimulates innovation through transfer and share of tangible and intangible resources; and combination and exploitation of complementary capabilities of competitor firms, particularly in knowledge intensive, dynamic, and complex industries (Carayannis and Alexander, 1999). Moreover, coopetition enables not only creation but also commercialization of innovation (Bouncken and Fredrich 2012), (Dagnino and Padula, 2002), Setbacks about Coopetition: Opportunism Threat and Trust Issue Alongside with academic studies emphasising and exemplifying benefits of coopetition, contradicting studies stressing on the disadvantages of coopetition also exist (Chin et al 2008), (Gyanwali et al. 2006), (Morris et al 2007). The majority of the negative concerns about coopetition are based on the threat of opportunism, claiming the likelihood of rivalry to hamper the firm s performance in a coopetitive relationship (Nieto and Santamaria, 2007), (Morris et al., 2007). The risk of critical knowledge leakage considered as one of the biggest threats, especially in terms of innovation-related coopetitive relations (Khanna et al., 1998), (Bayona et al., 2001), (Nieto and Santamaria, 2007). Moreover, Amaldoss et al. (2000) argued that the contradicting natures of competitors and threat of exploitation make coopetition affect innovation and technological development negatively. Another concern about coopetition is, regarding the difference in the learning paces and the targets of the involving firms (Dagnino and Padula, 2002), (Hamel, 1991), (Inkpen, 2000), the risk of the firm who has gained the targeted outcomes from the formation would leave before the other firm(s) set their expectations from the coopetitive formation. Trust is accepted as one of the most important factors for a coopetitive relationship to be successful (Akdogan and Cingoz, 2012), (Hamel, 1991), (Castaldo and Dagnino, 2009), (Devetag, 2009). Once trust is provided, firms would share and deploy their 18

29 resources into a coopetitive relationship, which would considerably affect the success and quality of the outcomes of coopetition (Gulati et al., 2000), (Chin et al., 2008). It is worth mentioning that, in spite of all risks and setbacks, it is possible to have positive outcomes from coopetition, once proper structures were provided and necessary actions were taken. Moreover, as (Bouncken and Fredrich 2012) claims, the positive outcomes of the effect of coopetition, particularly innovation, would outweigh all possible negative effects The importance of the coordinating organisation in Network Coopetition As previous section briefly demonstrates, trust carries utmost importance for success of coopetitive strategy. Nonetheless, trust should be strengthened with a legal structure, which would help maximizing the value created and minimizing the threat of opportunism (Abdallah and Wadhwa, 2009), (Gulati 1995), (Poppo and Todd Zenger 2002). In the presence of uncertainty and risk of opportunism, formal governing structure of a coopetitive network is essential for parties to be motivated towards involving such formation, and the continuity of the trustworthy environment where firms would utilize their resources for the collaborative value creation with competitors. However, the presence of a legal contract can guarantee neither the success nor the attractiveness of coopetitive formation. Especially in network coopetition, it is very likely that chaos to occur, regarding the contradicting interests of involving parties. In such situation, a coordinating mechanism would be essential, in order to prevent chaos and provide the smooth run of the coopetitive relationships. Bengtsson and Kock (2000) showed the importance of a network-coordinating organisation, in the case of Swedish Brewery industry. In such a case, an intermediate actor, for example, a collective association (such as the Swedish brewery association), is needed to coordinate and define how to compete or how to cooperate with each other. The intermediate actor thereby exhibits a formal logic of interaction collectively agreed upon. However, the role and importance of such intermediate actors, where this study refers as coordinating organisations remains 19

30 as an unaddressed issue in literature. Both case studies of this study exemplify advantages and importance of such coordinating organisations Comparing SMEs and large companies in terms of coopetition Another contribution of this study is the comparison it provides between SMEs and large companies, in terms of their approach towards coopetition. Augmented with case studies at the following sections, it is claimed that coopetition holds even greater importance for the SMEs, as coopetition becomes a necessity regarding their greater scarcities in terms of resource and capabilities. Compared to large companies, SMEs are more vulnerable to the external changes, regarding limited financial reserves, organisational capabilities, market presence, and customer base (Morris et al., 2007) (Levy et al., 2003). In contrast to large multinational enterprises, which can simply hire or buy such resources, entrepreneurial firms must seek resources supplied by external organisations (Lu et al., 2010). As the father of innovation Schumpeter (1942) claims, the survival of a company is only possible with innovation, and its ability to adopt the changes. Watanabe et al. (2009) also introduces the term being technopreneurial, claiming its importance in the era of mega competition. Regarding the weaknesses of SMEs mentioned above, it is possible to say that R&D is the most crucial area to coopete for SMEs. Arrans and Arroyable (2008) and Tether (2002) also claim that coopetition is the most beneficial in the high-tech areas. However, SMEs resources and capabilities would not be solely enough to be continuously adaptive and innovative (Akdogan and Cingoz, 2012). Indeed, SMEs have to race against time, in order to create innovation and recover their investments in short period of time, so that they could gain superior performance against their large and small-sized competitors (Narula and Hagedorn, 1999). Furthermore, innovation and R&D is an ambiguous process, as not any research guarantees to lead to an innovative discovery (Gnyawali and Park 2009). It is a likely case for a firm to invest big amount of money, spend years on a research, and getting no fruitful results in the end. For a large company, such case would be a significant financial loss. However, it might be the collapse of an SME, regarding its 20

31 scarce resources. All those reasons lead the conclusion that coopetition would be essential for survival of SMEs (Merrifield, 2007). Compared to dyadic coopetition, network coopetition would particularly be more fruitful for SMEs, as deployment resources of two SMEs might not be sufficient, neither. Within a coopetitive network, SMEs would reach scale and scope of resources. To summarize the advantages of coopetition for SMEs, they can share high costs, ambiguity and risks (Gnyawali and Park 2009), (Ritala et al., 2009), and shorten the innovation process via coopetition (Narula and Hagedorn, 1999). Moreover, they can reach economies of scale and scope (Gomes-Casseres, 1997), outmatch a stronger competitor, help entering new markets, and provide access to external resources (Barnir and Smith 2002). Another difference that literature detects between SMEs and large companies is that it is easier for SMEs to adapt coopetitive formations with their flexible structures. For large companies it is a more challenging task to adopt into a coopetitive formation, regarding their strict corporate structures and high level of bureaucracy with formal procedures (Gnyawali and Park 2009). 21

32 3. METHODOLOGY As Yin (1994) states, the fit of the research strategy depends on the factors such as type of research question(s) and whether it is focused on contemporary or historical phenomena and the control the investigator has over the events. Regarding the exploratory and descriptive inquiries this study carries on the coopetition concept, it adopts qualitative research. In terms of the research design, this study is divided into two main sections. In the first section of the study, with the motivation of providing theoretical contributions, previous academic studies were analysed. Subsequently, a clear definition of coopetition is provided, and a framework on the nature and advantages of coopetition were introduced. This first section provides a strong basis for the second section of the study, as it is not possible to explore the nature of a concept without clearly defining what it actually is and what its defining characteristics are. In the second section of the study, two case studies provided insights about the nature of network coopetition, and exemplified its advantages. In overall, this study seeks for the answers of the following research questions: 1. How is the nature of coopetition and what are the advantages of coopetitive strategy? 2. What is the role and importance of a coordinating organisation in network coopetition? 3. What are differences between SMEs and large companies in terms of their approach towards coopetition? 3.1. Case Study Design A case study is, with the definition of Yin (1994), an empirical inquiry that investigates a contemporary phenomenon within its real-life context, especially when the boundaries between phenomenon and context are not clearly evident. The main reason of choosing a case study over other methods is that the area is underdeveloped and has many gaps in the literature, and the boundaries of the concept are not clear. With the case study approach, it is expected to discover many aspects about the complex nature of coopetition. 22

33 This study adopts a multiple case study design, in order to demonstrate coopetition from a wider perspective, and to assess the importance of coordinating organisations in network coopetition with two different examples. By analysing primary and secondary data in a convergent and complementary manner, it is aimed to have triangulation among all types of data obtained. Triangulation is a rationale of using multiple types resources (Yin 1994), where it provides verification of the data gained through qualitative research (Osland, Osland, 2001). As figure 6 summarizes, a comprehensive research strategy is adopted, where interviews as primary data are combined with many other secondary resources such as company reports, company and organisation websites, industry reports, previous interviews and speeches of the Top Managers. Additional to providing a deeper and wider insight about the concept and its implications, it also served as the verification tool, as it provides the chance of measuring how consistent the obtained data with the other data resources is. Figure 6: Triangulation of the Research INTERVIEWS FROM DIFFERENT LEVELS NEWS, ARTICLES PUBLISHED REPORTS WEBSITES 23

34 Interviews Interviews are accepted as irreplaceable sources in case studies (Yin 1994). Parkhe (2004) claims that they are great opportunities to tap into the brain of the people, in order to see their motivations and expectations in decision-making processes. In this study, indeed, it was aimed to tap into the brains of the people who made the decisions about entering a coopetitive formation, who manage coopetitive relationships and who design and operate the coopetitive relationships of networks. Primary data of both cases were obtained through interviews conducted with officers and managers from different levels. The reason of interviewing people from different levels has been the endeavour of approaching the concept from different perspectives, and correspondingly having deeper insights about the nature of coopetition. As Welch et al. (2002) mentions, top managers are key people for gathering information; however, hierarchically lower level people sometimes provide even more in-depth information (Macdonald and Hellgren, 1999). In the Turkish Airlines Case, for instance, interviews were conducted with the General Manager of Alliances, an officer who is responsible for the coordination of alliance relationships, a regional general manager, and a regional marketing manager. In addition to interviews conducted directly related with case studies, two additional interviews were conducted at the preliminary stage of this study, carried out by the motivation of gaining more insights about coopetition. One formal and one current representative of the SME Development Agency, the biggest SME-supporting organisation of Turkey were interviewed about a subsidizing programme that the agency provides for SMEs, which aims to stimulate coopetition on manufacturing among SMEs. Highlights of the interviews are mentioned at the very end of this study, as a suggestion of future research. Interviews were conducted either face to face, or in the form of a teleconference, lasting for 30 to 90 minutes. All interviews were recorded with the interviewee s permission. In order to provide richer insights for further research, all interviews are transcribed and provided as appendices (appendix 2 to 6). Indeed, interviews conducted in Turkish are provided in original language, and translated in English. 24

35 Moreover, except the representative from the SME Development Agency, all interviewees allowed their names to be publicly published. Considering the exploratory and descriptive inquiries that interviews carry, it is aimed to provide the interviewees flexibility to shape the flow of the interview in a conversation-like, open-ended structure. However, regarding the limited time allocated for the interviews (interviewees are busy people), focused type of interviews were chosen as the best fit. In focused interviews, interviews remain open ended, however the interview is led by the set of pre-determined questions (Merton et al., 1990). Indeed, two interview sessions (interviews 3 and 4-table 4), two participants were interviewed simultaneously. This also provided great opportunity to observe the conversation/discussion between two participants, and provided deeper insights. 25

36 Table 4: Table of Interviews CASE STUDY INTERVIEW NUMBER NAME POSITION Cited As TURKISH AIRLINES Interview 1 Serhat Sarı Turkish Airlines, Scotland General Manager (Sari,2013-Interview 1) Interview 2 Fatma Basaran Çiçek Turkish Airlines Edinburgh- Regional Commercial Manager- Turkish Airlines (Cicek, Interview 2) Edinburgh Directorate Interview 3 Onur Alpan Turkish Airlines Manager- International Relations and Agreements Interview 3 Banu Ekerim Turkish Airlines International Alliances Specialist EUREKA Interview 4 Marej Jazak Impact & Portfolio Analyst ar EUREKA Secretariat (Alpan, Interview 3) (Ekerim, Interview 3) (Jazak, Interview 4) Interview 4 Piotr officer at EUREKA (Pogorzelski, Pogorzelski Secretariat Interview 4) (Yurttagul, Interview 5) (Kaplan, Interview 6) (Anonymous,2013- Interview 7) Background Interviews: SME Development Agency- Turkey Interview 5 Emre Yurttagül EUREKA Turkiey- International Project Coordinator Interview 6 Bahadır Kaplan Former SME Development Agencey Representative Interview 7 Anonymous SME Development Agency Representative 1

37 Case One: EUREKA The EUREKA case carried utmost importance in terms of observing the nature of network coopetition in R&D, which is one of the most popular areas of coopetition; and provided the opportunity to compare the SMEs and large companies in terms of their approach and motivations towards coopetition. Moreover, it had given great evidence in terms of observing the role of intermediate organisations in the success of coopetition. As primary data, 3 participants were interviewed. Two of them are from the EUREKA headquarter, Brussels-Belgium, and one of them is an experienced project coordinator from Turkey, which had the EUREKA Chairmanship with the main theme of coopetition. As secondary data, the websites of EUREKA, EUREKA Clusters, and EUREKA s Eurostars Programme websites, related reports, published documents and legal agreement templates have been the main resources Case Two: Turkish Airlines As it was mentioned in the previous sections, the reason of choosing the airline industry was that it is possible to observe coopetition in many areas among airline alliance members, where airline alliances are dominant actors in industry and competing against each other. In the Turkish Airlines case, the process of joining the biggest airline alliance, its advantages and disadvantages of being involved in such a coopetitive formation were analysed. Moreover, the importance and role of Star Alliance as the coordinating and intermediate organisation had been observed The analysis of interviews Interviews, as recommended by Miles and Huberman (1994), are analysed through the thematic approach where the pre-determined themes are used to channel the questions, as mentioned in table 5. 2

38 Table 5: Thematic Approach on Interviews TURKISH AIRLINES Company Characteristics Strategic positioning and the goals of the company Global Airline Industry Motives Behind Joining the alliance Advantages and disadvantages of the alliance Importance of Star Alliance to coordinate coopetition Competitor relationships while coopeting EUREKA Organisation information Trust issue in coopetition Importance of EUREKA in terms of coordinating coopetition Differences between the coopetition of SMEs and large companies About Eurostars and Clusters Advantages ad Challenges of Coopetition The future of coopetition The future of coopetition 3

39 3.3. ETHICAL CONSIDERATIONS This study was conducted with the ethical considerations in line with the University of Edinburgh Ethics Guidence. In table k, ethical attitudes introduced and grouped by Diener and Crandall (1978) are matched for this study and summarized in table 6. Table 6: Ethical Issues and the reflections of this study ETHICAL ISSUES by Diener and Crandall (1978) Whether there is harm to participants Whether there is a lack of informed consent Whether there is an invasion of privacy APPROACH of THIS RESEARCH Participants had no harm. None of them were forced to share any information which would put them into a contradictory position with their company/organisation, or which would jeopardize their position within the company or the organisation. All participants were fully informed about the purpose of the research, and claimed that the finalised version of the study can be shared with them once it s finished. The interviews were recorded with the interviewee s permission. Interviewee s names are used with their permission. One of the interviewee preferred to be kept anonymous. Whether deception is involved No deception was involved. Only the data which is permitted to be used is used. 4

40 4. CASE 1: EUREKA EUREKA is an international collaboration platform, focusing on supporting the research, development, innovation, and commercialization for market-oriented products and services in short run. The platform was founded in 1985 with the involvement of 18 member countries, and the European Union as the 19 th member. The main motivation for the establishment of such an organisation was to strengthen Europe against the increasing level of R&D in Asia and North America (Eureka website). The platform so far has supported more than 4000 R&D projects, and currently has 41 members, including the European Union (Appendix k). EUREKA supports research, development and innovation (thereafter R&D&I) projects by bringing small and medium-sized enterprises (thereafter SMEs), large companies, universities, and research institutes together. The reason of including EUREKA into this study is that, it is possible to observe innovation-based network coopetition, where both large companies and SMEs are involved-separately or together. Coopetition is a central concept in all EUREKA projects. As such, the main theme of the Chairmanship of EUREKA had been coopetition. As EUREKA Chairman Okan Kara declares, it is aimed to make EUREKA a flexible platform for coopetitive innovation (Kara, 2012). It is possible to classify EUREKA s activities in terms of dyadic and network coopetition structures. Individual projects are dyadic coopetition platforms, whereas Clusters, Umbrellas, and Eurostars Projects are coopetitive networks (figure 7). Within individual projects, two firms come together for an R&D&I project. EUREKA Clusters are 5

41 coopetitive platforms dominated by large firms, and aimed to lead industry-shaping innovations and market standardization. Umbrellas are thematic structures, where companies, research institutions, and related organisations take collective initiatives to facilitate the creation of more EUREKA R&D&I projects in specific sectors (Appendix t). Eurostars Programme is particularly dedicated and designed for SMEs, aiming to lead innovations within a coopetitive network. Within this case, EUREKA Clusters and Eurostars programme will be analysed and compared; in order to have deeper insights about network coopetition and its effects on innovation; and to analyse the differences of coopetition for SMEs and large companies. Figure 7:Eureka Projects as Dyadic and Network Coopetition Formations DYADIC Individual Projects NETWORK Eurostars Program EUREKA Clusters EUREKA Umbrellas EUREKA shows utmost care on the development of the SMEs in Europe, particularly the R&D intensive ones, aligned with the importance given on SMEs by the European Union (Eurostars Annual Review, 2011). As the Directorate General Enterprise and Industry of the European Union declares; more than 99% of the European businesses are small and medium sized enterprises. Moreover, SMEs provide more than two-third of the jobs in the private sector and create more than 50% of the value-added business activities within the EU (EU Directorate General, 2013). That is why; SMEs are considered as the backbone of the European economy, and are given utmost importance in the EU s agenda, so does EUREKA. As illustrated in figure 8, majority of the organizations participating in EUREKA Projects are SMEs. It is also worth mentioning that this study adopts the SME definition of the EU, which is summarized at the table 7 below. 6

42 Table 7: SME definition by the European Union Company Category Employees Turnover Or- Balance sheet total Medium-sized < m 43m Small <50 10m 10m Micro <10 2m 2 m Resource: EU DG, 2013 Figure 8: Distribution of Organizations Participating in EUREKA Projects Number of Organizations Participating in Eureka Projects 29% 15% 2% Resource: EUREKA 2011 Report Figure 9: Participants in Eurostars Projects 54% SMEs Large Company University and research institutes Other Type of participants in EUROSTARS approved R&D performing SME University Research Institute Large Company other 11% 7% 1% 13% 68% Resource: Eurostars Website 7

43 Figure 10: Types of Eurostars Consortiums SMEs only Types of consortiums in terms of participants SME + 1 Research Organisation, or University SME+more than 1 Research Organisation or University 20% 15% 28% 37% Resource: EUREKA Website 4.1 Network Coopetition in Eureka Eurostars Programme: SMEs in Network Coopetition In the Eurostars Programme, competitor SMEs come together in a coopetitive formation, by deploying their resource and capabilities and share the risks and benefits of the R&D&I endeavours. Indeed, those projects are international coopetitive platforms, as a minimum of two participants have to be from different participating countries. Additional to SMEs, research organisations, universities, and large companies also might join the Eurostars Projects (figure 10). The programme was originally founded with the budget of 400 million Euros, which of 75% from EUREKA member countries, and the rest is from the 7 th Framework Programme of European Union: the main programme dedicated on the development of SMEs and Innovation in the EU. As the successor of Eurostars Programme, Eurostar2, which is the successor of the 7 th Framework Program, will be in force by 2014 to (Eurostars Annual Review, 2011). The process of being involved into a Eurostars Project evolves as follows: First candidate SMEs apply with their project idea. After the submission, the project gets evaluated by EUREKA. In case of the project is approved, national funding bodies connected to EUREKA fund the project, as the national funding bodies are the primary fund resource. (figure 11). 8

44 Figure 11: Eurostars Project Approval Process SMEs apply for the project submit application to EUREKA project evaluation by EUREKA approved projects apply for national funding Since its announcement by the Research Commissioner Janez Potonik in October 2007, Eurostars plays a catalyser position for SME coopetition in R&D&I in an international platform. It does not only aim to develop but also to commercialize new ideas, services, and products. (Eurostars Annual Review, 2011). The projects are required to be market driven, where projects have a maximum of 3 years duration and are required to be ready to be launched in the market within the 2 years of project completion (except projects requiring trials such as biomedical or medical projects) (Eurostars website, 2013). With its flexible and close to market approach, this coopetitive programme is claimed to be the ideal model for the future of the national/international research programmes (Eurostars Annual Review, 2011) Eureka Clusters EUREKA Clusters are long term strategic formations. They are networks governed and coordinated by leading large-sized industry firms. Regarding their potential benefits and outcomes, the primary goal of these clusters is ensuring the leading position of Europe in technology and innovation (eureka website). Clusters have two main objectives: Developing generic technologies for the industry, and setting industry standards in Europe. Information and communication technologies (ICT), energy, and biotechnology are the most active R&D&I areas of clusters. 9

45 At the table 8, you can see a list of EUREKA clusters. As Pogorzelski claims(2013, Interview 4); Catrene, Celtic Plus and ITEA are the three most active clusters. Table 8: EUREKA Clusters CLUSTER NAME ACQUEAU INDUSTRY Water Technologies CELTIC+ Telecommunication, mobile technologies and internet infrastructures EUROGIA CATRENE EURIPIDES Renewable Energies ICT: Micro and Nano Electronics ICT: Smart Integrated Systems ITEA 2 ICT: Software solutions, service software, e- health, firmware MANUFUTURE INDUSTRY Manufacturing systems and technologies Resource: Eureka website Clusters: Large Companies in Network Coopetition As EUREKA Chairman Okan Kara declares, clusters are great source of coopetition (Kara, 2012). Within cluster projects, actors share risks and benefits of R&D&I endeavours, and aim to the development and exploitation of the technologies created. It is possible to see three different forms of coopetition within clusters: 1) Industry leader large companies coopete for setting industry standards 2) Large companies coopete for R&D&I 3) Large and small companies coopete for R&D&I 10

46 Figure 12:Eureka Clusters and forms of coopetition coopete in R&D&I clusters Coopetition between large companies only determine industry standards open calls for cluster projects Coopetition between large and small companies In some projects research institutes and universities are involved as well Each cluster has a technological roadmap, where the needs and the challenges of the industry are defined, and the technological areas that are needed to develop are mentioned (ITEA 3 Booklet, 2012). Those roadmaps are created by the board of management of the cluster, which consists of the leading big companies of the industry (Yurttagul, EUREKA Turkey, National Project Coordinator. Interview 5). Roadmaps are flexible and continuously adapt to the technological changes and the needs of both the markets and the society. In order to have a multidisciplinary approach for innovation, there is a collaborative formation between clusters, an intercluster committee where all EUREKA Clusters are represented in a rotating chairmanship structure (ITEA 3 Booklet, 2012). Clusters periodically open calls for the projects and collect applications of project proposals from companies with different sizes: SMEs and the large ones, accompanied by universities and research institutes. Cluster projects are expected to 11

47 be a good mixture of large, important companies, SMEs and academia (Handbook, 2011). After the assessment process, successful candidates receive the cluster label. Once the project gets the cluster label, the members of the cluster apply to their related national funding organisation in their home countries (table t). The funds are orchestrated by the cluster, and provided by the public authorities from EUREKA member countries (Eurescom, 2012). Additionally to the outsider applicants, the governing big cluster members also might introduce projects, or participate in the projects presented at the calls. Figure 13:The process of cluster projects firms apply to clusters for their project submit application project evaluation by Cluster approved projects receive cluster label apply for funding to national bodies 4.2 Analysis of the Programmes The previous section gave a brief introduction about Eurostars Programme and Eureka Clusters. In that section, the advantages of network coopetition within those programmes, and the importance of EUREKA as a coordinating and regulating mechanism will be assessed. After that, the differences between SMEs and large companies in terms of coopetition will be analysed Advantages of Eurostars and the Clusters Advantages consistent with the Literature Review of Coopetition When both programmes were analysed, it is possible to say that firms enjoy the benefits of network coopetition in terms of innovation and learning, cost related and market related advantages. Referring back to the figure 4 from the literature review section, it is possible to place the advantages listed at that section within EUREKA networks, as well (figure 14 ). 12

48 Both Clusters and Eurostars Programme stimulate knowledge sharing, new knowledge creation and innovation stimulation. Indeed, involving parties share the risk and cost (although projects are funded, finance might be needed at the initial stage). Additionally to the common advantages, Eureka Clusters also enjoy the benefits of market standardization and lobbying, which will be mentioned in details later. Figure 14: Advantages of coopetition mentioned at the literature review COST RELATED CLUSTERS bargaining power economies of scale cost sharing CLUSTERS EUROSTARS market standardization, lobbying advantages of coopetition risk sharing EUROSTARS CLUSTERS CLUSTERS knowledge share increased innovation and learning EUROSTARS EUROSTARS CLUSTERS CLUSTERS Additional advantages related to the existence of a coordinating organisation Furthermore this study comes up with other advantages of network coopetition that involved parties enjoy, which are directly related to the existence of a coordinating 13

49 organisation; which is the EUREKA Organisation itself. Those advantages will be assessed in details, and can be listed as followed: EUREKA provides the framework of the necessary structure needed for the smooth running of coopetition, and provides support and counselling on these manners. With the legal structure it requires the network to build and minimize the threat of opportunism and trust problem of involved parties. Being recognized as a EUREKA project provides a certain level of prestige. It facilitates access to the necessary institutions, and provides access to funding EUREKA helps finding partners to coopete, and stimulates international partnerships Running Coopetition Smoothly and Solving the Trust and Opportunism Related Issues Once all primary and secondary data is analysed, it turns out that the requirements candidate projects have to comply with do not only serve the purpose of choosing the best promising projects, but they also serve the purpose of realizing the smooth running of coopetition. Indeed, the legal structure that the project has to provide minimises the threat of opportunism and helps solving the trust-related issues, by making the projects built on a strong legal basis to protect the firm-specific knowledge and the property rights of the outcome of the coopetitive project (figure 15).. 14

50 Figure 15: Consortium Requirements for Successful Coopetition PROPERTY RIGHTS MANAGEMENT Consortium Non-disclosure agreement GET READY TO COOPETE & GET SUCCESSFUL RESULTS RISK MANAGEMENT CONFLICT MANAGEMENT Define risks Cover-up options define decision making and conflict resolution procedures PROJECT MANAGEMENT Define roles and responsibilities Minimising the Threat of Opportunism and Solving Trust-related Issues As it was discussed at the literature review section, almost all negative aspects about coopetition seem related to the lack-of trust between partners. Once partners do not trust each other regarding the threat of opportunism of competitors within a coopetitive network, they either do not enter such formations or even if they are already involved, they restrict the resources and capabilities shared with competitors, which prevents getting optimum results from such relationships. In order to solve these issues within EUREKA projects, Consortium Agreements carry utmost importance. The very first thing that all interviewees mentioned to the question how trust is achieved and how the ideas are protected was Consortium Agreements (Zajak &Pogorzelski Interview 4, and Yurttagul, 2013-Interview 5). Indeed, a strong and convincing consortium is a must for the project of getting approved (Handbook, 2011). 15

51 Consortium Agreements are required to define clearly the involved parties, their rights and responsibilities, and protection of property rights about the new product to be created in the end of the project. The companies that are working in a given project, before they receive funds and before the project is even approved, they have to define in a certain extent that how they are going to deal with sharing the things that they create together (Zajak, Interview 4). Building a Consortium Agreement, in other words, forming the structure of coopetition, is a back and forth process, where firms are constantly in touch with a national representative of Eureka, who counsels them in every aspect of providing necessary formation and structures (Pogorzelski 2013, Interview 4). In addition to the Consortium Agreement, a Non-Disclosure, or Confidentiality Agreement is another mandatory requirement for each project application. These agreements provide the assurance that no sensitive information will be shared with any other parties; and that in case the project proposal does not succeed or a partner to step out, the confidential information will not be further-used in a non-authorised or in a damaging way (Interview 4 and 5),. Additional to all the legal agreement framework, EUREKA advices all involving parties to get to know about the basic concepts of intellectual property rights. At the appendix, you can find confidentiality agreement and the skeleton for a EUREKA Consortium and the checklist for provided for the formation of these agreements. Providing the blueprint of the governance: Smooth governance and how to solve the conflicting issues For both Eurostars and Cluster Project application processes, it is also mandatory to provide a sound project-management structure. By doing so, EUREKA forces involved parties to create the necessary structures for the smooth running of the coopetitive process. It is expected to clearly define a management structure, which provides the roles and responsibilities about the project coordination, administrative handling, technical coordination, and operational management. However, it is mentioned that this structure should assure efficiency, but should not be overstraining (CelticPlus, 2011). 16

52 Additional to the project management, it is also expected that the project provides a sound structure in terms of managing possible conflicts. Regarding multiple competitors are involved in a coopetitive framework, it is very likely to have conflicts and those are needed to be efficiently managed to make project reach its ultimate goal of creating an innovative product. As such, EUREKA requires the candidates to provide a conflict management structure, where decision making and voting procedures are defined in addition to a conflict resolution plan. Regarding R&D&I projects involved risks, it also requirea projects to have a strong risk management structure. That is why, it is mandatory to clearly disclose the potential risks and the cover-up options related to those risks. Once those requirements are complied, it means that the candidate project has: - A management structure to keep the smooth running of the project. - A strong legal structure to protect the property rights, and firm-specific information. - Awareness of the risks of the projects and plans for risk recovery. - A strong framework to solve possible conflicts during the projects. Prestige Involving in a coopetitive formation via EUREKA provides a certain level of prestige, as having a project approved by EUREKA requires carrying a significant level of capabilities, and satisfaction and a certain level of quality standards (appendix k for the standards required). Once the project application is approved by EUREKA, the project receives the EUREKA label, which is perceived as a symbol of prestige. As it is a proof of the project s quality, regarding the project has passed EUREKA s rigorous assessment procedures; the label enhances visibility and serves as a source of confidence for the potential investors. A Eurostars Project, FlexGen s Chief Scientific Officer Joop Van Helvoort mentions in an interview that, having their project approved and partly funded by a European Programme helped them a lot to get the rest of the money from investors (CITE MAKE SURE). Another Eurostars Project, CrossJect s Chief Technology Officer Patrick Alexander mentioned in an interview that Eurostars 17