All the information, tables and figures provided in this report are reserved and cannot be used without reference.

|

|

|

- Berna Toraman

- 8 yıl önce

- İzleme sayısı:

Transkript

1 All the information, tables and figures provided in this report are reserved and cannot be used without reference. T.R. ENERGY MARKET REGULATORY AUTHORITY Petroleum Market Department ANKARA, 2013

2 MESSAGE FROM THE CHAIRMAN Turkish petroleum sector has seen a rapid growth especially since 2005 when Petroleum Market Law no.5015 was enacted and Energy Market Regulatory Authority was authorized for regulating and auditing the petroleum market. Political and economic stability has brought about steady growth and all activities in the sector were registered. In the same period, unregistered, illegal or illicit fuel problem was reduced significantly. Licensing process finalized by the Authority within this period has played a significant role in registering market players and reducing the number of unregistered activities in the market. As a result of these, competition in the sector increased, new players joined the market and quality, product and service range improved. A general overview of the petroleum sector in 2012 reveals that petroleum sector continues to be a center of attraction for investors where entries into the sector accelerate, storage capacities increase, refinery improvement and establishment activities continue. Some of the positive developments in the sector in 2012 were that the companies in the sector were also the focus of attention in financial markets, oil industry companies ranked as the largest Turkish companies and especially towards the end of the year, new foreign companies entered the market. As the Energy Market Regulatory Authority, we are responsible for undertaking activities in the dynamic petroleum market efficiently within public liability. By attending various national and international meetings, we have the opportunity to closely monitor the petroleum market and become familiar with future projections. Since 2005, we have been sharing the annual market reports with the public regularly, continuously improving the content. By preparing monthly versions of this annual report since last year, we have enriched the content with up to date interpretation of data provided. In 2012 Petroleum Market Report, rather than simply discussing tax, price or unregistered activities in the petroleum industry, we also provide data on certain fields such as the petroleum market s contribution to national economy and employment figures in the market. With this, we aim to present the role of the sector in macro economy Petroleum Market Report, prepared in line with our understanding of continuous research, learning, improvement and innovation, is a substantial outcome of this understanding. I congratulate all Petroleum Market Department staff who contributed to the preparation of this report. I wish this report will be beneficial to all parties concerned. Hasan KÖKTAŞ Chairman

3 FOREWORD Petroleum Market Sector Reports aim to provide detailed information on all petroleum activities in the market, analyze national and international developments influencing the sector, enable comparisons wit previous years and help shaping future projections of petroleum industry. When the Petroleum Market Sector Report prepared with this aims within the scope of international reporting principles and standards is evaluated regarding the scope of data included, it stands out as the only source in Turkish petroleum market. The Report, prepared as a result of detailed and careful studies this year as in the previous years, makes 2012 data available to all readers. The economic magnitude of our sector, local and foreign investors interest and the competition in the sector continue to increase every year. Therefore, access to complete and accurate data is essential both for the state institutions and organizations and for the private sector. Petroleum Market Report displays the change and development that the petroleum sector has undergone in the recent years. With the same sensitivity in the upcoming periods, our reports will be shaped and improved in line with the requirements. I wish 2012 Petroleum Market Sector Report, which has been awaited by the public, interested parties, local and foreign investor, will be beneficial to all stakeholders and express my thanks to Petroleum Market Department staff for their efforts in the preparation of this report.

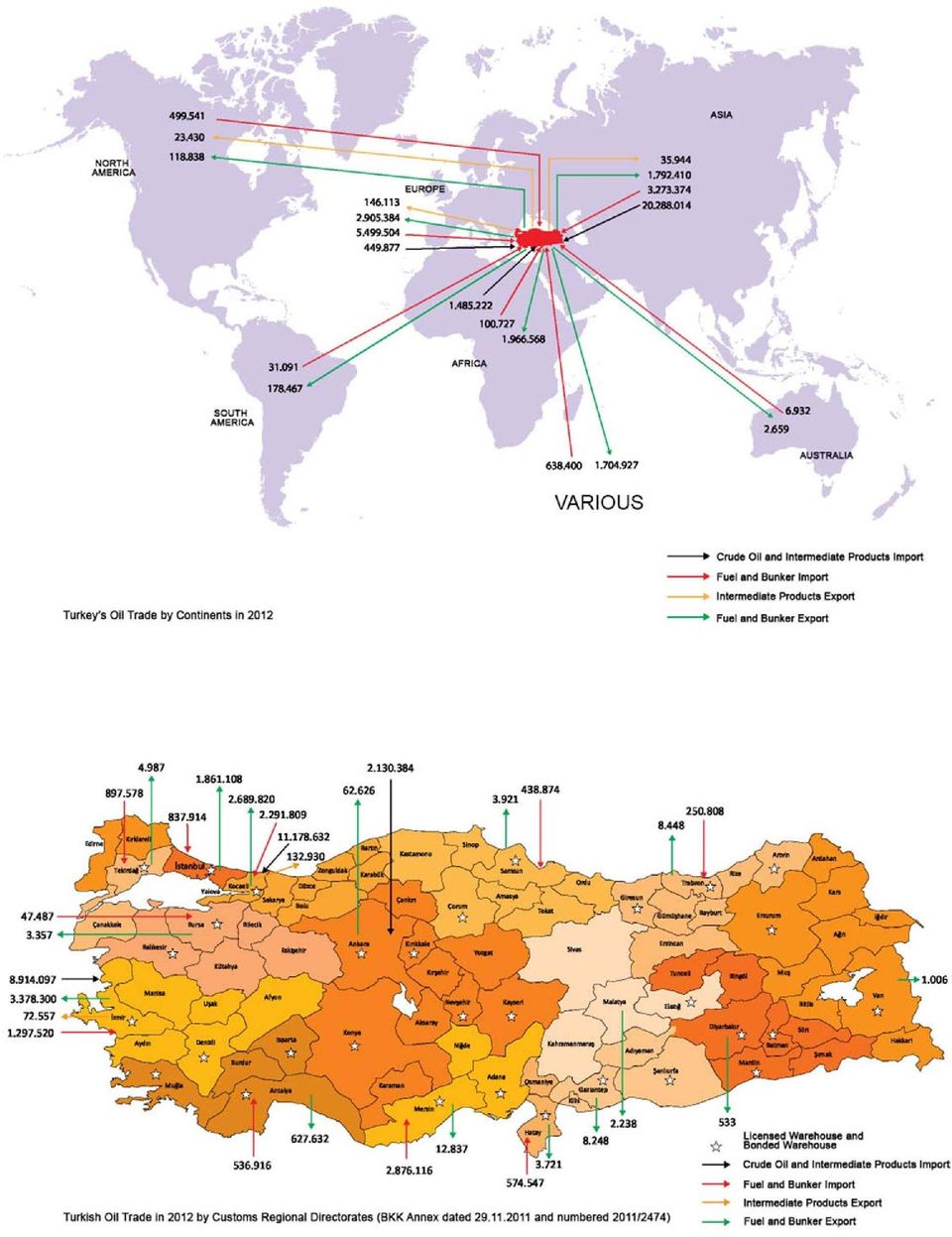

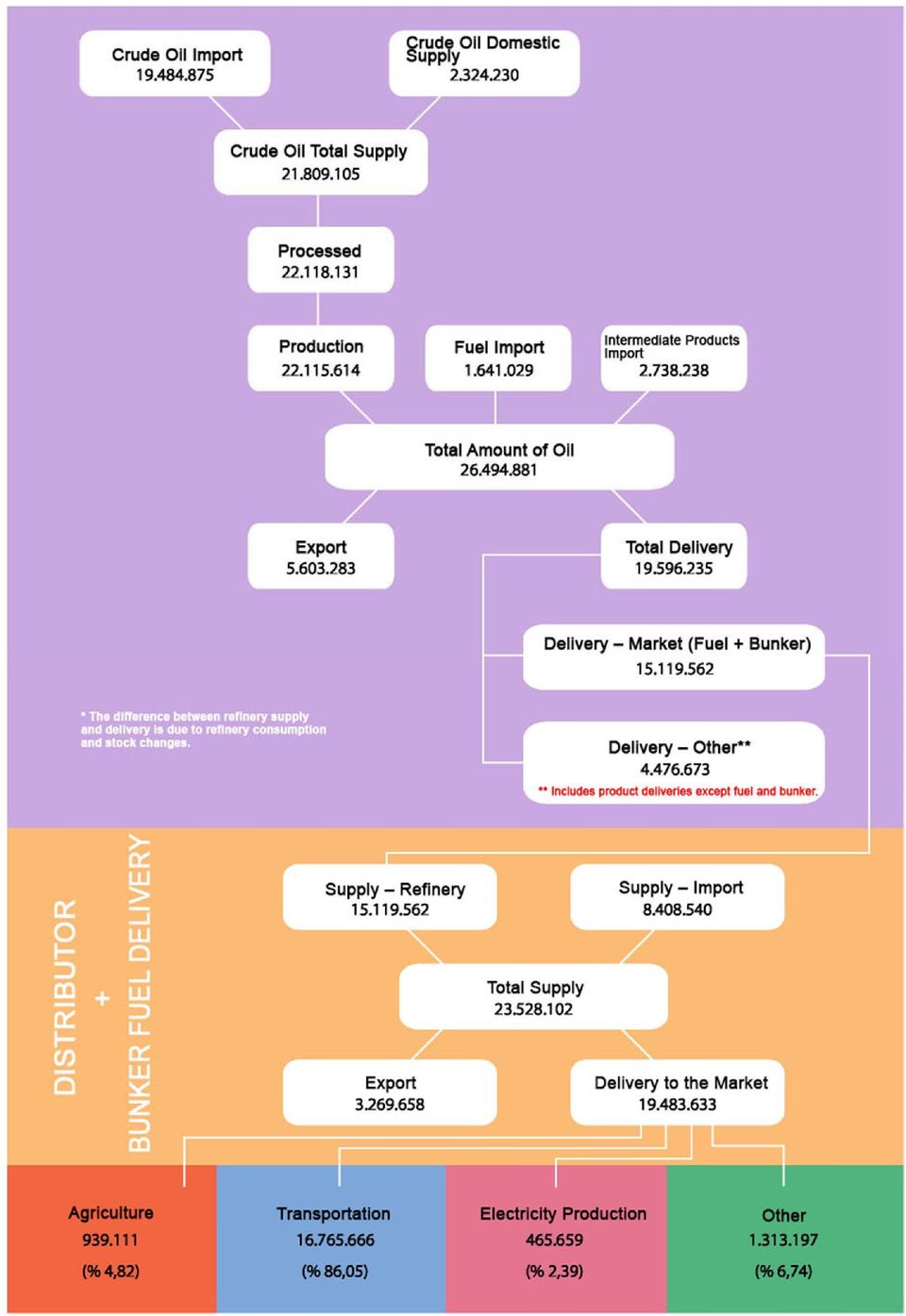

4 EXECUTIVE SUMMARY Refinery utilization rates have constantly increased in the last three years and refinery utilization rates (excl. Intermediate products) were 68.4% in 2010, 74.8% in 2011 and 78.7% in While imports in total crude oil supply of refineries has an upward trend, supply from domestic production has a downward trend on the contrary. A natural outcome of this situation is being more and more dependent on foreign sources in crude oil supply. Foreign source dependency rates in 2010, 2011 and 2012 were estimated as 86.9%, 88.1% and 89.3% respectively. In addition, only 11% of the crude oil used by refinery license holders was procured from domestic production in 2012 while nearly all the rest was imported from Iran, Russia, Iraq, Saudi Arabia, Kazakhstan and Libya. In 2012, Libya became one of the countries from which crude oil is imported. The average price per barrel of crude oil imported in 2012 was 111 US Dollars per ton. When the distribution of end products produced by refinery license holders is analyzed, it is observed that in 2012 the share of Fuel Oil Types decreased to 4.9% from 11.8% and the share of diesel increased to 35.2% from 33.4% compared to In 2012, 18,366 tons of autobiodiesel was sold to distribution license holders by only 1 processing (biodiesel) license holder. The number of processing license holders continues to decrease for the last three years; while there were 45 processing license holders in 2010, there were 36 in 2011 and 25 in The amount of liquid fuel and bunker products supplied from refineries by distribution license holders in 2012 totaled 10.8 million tons. The amount of products (liquid fuel and bunker) imported by distribution license holders in the same period totaled 8.4 million tons. When the import figures of distribution license holders in 2012 is analyzed, it is observed that approximately 85% of import was carried out by top 5 companies. In addition, diesel import constituted 92% of total import. Approximately two thirds of the products were imported from India, Italy and Greece by distribution license holders. The amount of liquid fuel traded between distributors in 2012 totaled 1.85 million tons and diesel types constituted 88% of total sales. While the downward trend in gasoline and fuel oil types sales and the upward trend in diesel types sales of distribution license holders continues, total liquid fuel sales reached 18.2 million tons in 2012 with an increase of 3.8% compared to the previous year. The amount of fuel sales by distribution license holders through Vehicle Identification System (VIS) totaled 135,000 tons (120,000 tons of unleaded gasoline and 15,000 tons of diesel fuel). Sales through VIS constituted 8.5% of total fuel deliveries to vendors. It is observed that the concentration in distribution license holders liquid fuel sales market has a downward trend, the total market share of top 10 distribution license holders with largest market shares in liquid fuel sales in 2010, 2011 and 2012 were 87%, 83.4% and 82.9% respectively. HHI values applied for market concentration estimations verify the downward trend in concentration level. On the other hand, market share rankings of the top 10 companies with largest market shares have changed. In addition, it is observed that fuel sales have a seasonal trend, sales of Gasoline and Diesel types that peaked in July fell to its lowest level in January February while there was an opposite trend in Fuel Oil Types.

5 The amount of liquid fuel delivered to vendors by distribution license holders totaled million tons in 2012 and the amount delivered to vendors constituted 93% of total distributor sales. 8 per mille of total vendor sales were made through vendors without stations. The amount of sales to eligible users was 1.08 million tons and diesel types constituted 71% of the sales. When the sectoral breakdown of sales is analyzed, it is observed that approximately 86% of total sales in 2012 was for transportation purposes, 2.4% for electricity production and approximately 5% was for agricultural purposes. When bunker supply sources of bunker delivery license holders (including holders of distribution license with bunker delivery subtitle) are analyzed, it is observed that almost all of the imports (424,726 tons) were jet fuel and airplane gasoline and that there were no import activities regarding bunker supply for marine fuel deliveries. Marine fuel sales to the domestic market totaled 500,000 tons and most of the sales were diesel types sales. It is observed that 2 companies with largest market shares carried out half of the sales. The amount of sales of marine fuels purchased from refineries on export basis and sold to sea vehicles within export regime totaled approximately 830,000 tons and 5 companies with largest market shares carried out almost all of the sales. The amount of sales to sea vehicles subject to transit regime totaled approximately 1,325,000 tons. Therefore, total bunker fuel sales to sea vehicles amounted to 2,655,000 tons in It is observed that 95% of inland bunker fuel deliveries were SCT free and that the market is highly concentrated in terms of both domestic deliveries and deliveries within the scope of export regime. Aviation fuel sales to the domestic market totaled 810 thousand tons and nearly all of the sales were jet fuel sales. The amount of sales of aviation products purchased from refineries on export basis and sold to aircrafts within export regime totaled approximately 2.5 million tons. It is observed that 3 companies with largest market shares carried out almost all of the sales in both fields. The amount of sales to aircrafts subject to transit regime totaled approximately 80 thousand tons. Therefore, total bunker fuel sales to aircrafts amounted to 3.39 million tons in It is observed that aviation bunker delivery market has a more concentrated structure compared to marine bunker fuel market and that competition is considerably limited. Total bunker sales (aviation and marine) from Turkey totaled approximately 6 million tons. Storage capacity for providing service to third parties under storage license increased by 3.5% in 2012 compared to 2011, totaling 4 million 861 thousand m3. With the storage capacity of refinery license holders, total storage capacity reached approximately 10.4 million m3. Based on data provided by distribution license holders on 8,966 vendors, it is observed that the total number of employees in vendors is 46,591 (88% employed in fuel delivery) and that the average number of staff per vendor is 5.2. When distribution license holders average fuel delivery figures per vendor are analyzed, it is observed that average sales per vendor of 5 distribution license holders with largest market shares in total shares is also above Turkey average (1,322 tons/vendor). Total sum of indirect taxes collected from gasoline, diesel and fuel oil types (excl. bunker deliveries) in 2012 is estimated as approximately 43.5 billion TL. This sum constitutes 13.2% of total tax revenue Petroleum Market Sector Report covers information on the following topics in addition to the topics covered in the previous years reports: Sectoral breakdown of liquid fuel sales by distribution license holders, Number of staff employed by vendors, Number of vendors of distribution license holders by cities ( listing fuel vendors with and without stations, bunker fuel vendors with and without stations), Relationship between vendor numbers and market shares of distribution license holders.

6 EXECUTIVE SUMMARY TABLES

7 Product (ton) Gasoline Types Diesel Types Fuel Oil Types Marine Fuels Aviation Fuels PETROLEUM MARKET OUTLOOK (ton) Refinery Production Refinery Import Distributor Import BDLH* Import Distributor Bunker Export BDLH* Bunker Export Refinery Bunker Export Distributor Fuel Export Refinery Export Distributor Sales** Other Refinery Sales*** Other Distributor Sales *** Distributor Bunker Sales *** Total TOTAL *BDLH stands for Bunker Delivery License Holders. ** Includes sales with and without VAT to eligible users in the market, license holders deliveries to their vendors (incl. VIS), SCT free sales in the market except bunker sales; excludes sales in the form of military deliveries. ***Military Sales are included. BDLH* Bunker Sales

8

9

10 CONTENTS 1. OIL IN THE WORLD 1 1. Oil in the World World Oil Demand World Oil Supply World Refining Capacity 6 2. OIL IN TURKEY 9 2. Oil in Turkey Refining Activities Processing Activities Distribution Activities Bunker Delivery Activities Vendor Activities Eligible User Activities Lubricant Activities Storage Activities Transmission Activities 123

11 3. PRICE MOVEMENTS Price Movements in the Mediterranean Region and Import Prices in Turkey Domestic Price Movements Unleaded Gasoline 95 Octane Price Movements Diesel Price Movements Heating Oil (Sulphur level between %0.1 and %1) Price Movements High Sulphur Fuel Oil (Sulphur level above %1) Price Movements Fuel Prices in the European Union Storage Tariffs Transmission Tariffs FUEL QUALITY, AUDIT AND LEGISLATION STUDIES National Marker Implementation Establishment of Accredited Laboratories Vendor Automation System Technical Arrangements Other Legislative Arrangements Audit Activities 172

12 LIST OF TABLES Table 1. 1 World Oil Demand (million barrels/day) 21 Table 1. 2 Petroleum Products Consumptions in the World (million barrels/day) 22 Table 1. 3 World Oil Supply (million barrels/day) 23 Table 1. 4 Primary Countries in Crude Oil And Liquid Fuel Production in Table 1. 5 Number of Refineries in Table 1. 6 World Refining Capacity by Regions (million barrel/day) 25 Table 2.1 Definition of Petroleum (Crude Oil and Products) according to HS Code 28 Table 2.2 Refinery License Activities (unit) 30 Table 2.3 Information on Refineries which are not active yet 30 Table 2.4 Capacity Information on Refineries which are not active yet 31 Table 2.5 Capacity Utilization Rates Between (ton)* 32 Table 2.6 Crude Oil Import of Refinery License Holders between by countries (1.000 tons) 33 Table 2. 7 Petroleum Products Production of Refinery License Holders between) (ton) 35 Table 2. 8 Production Amounts of Refinery License Holders in 2012(ton) 35 Table 2. 9 Petroleum Products Import Amounts of Refinery License Holders by years (ton) 38 Table Petroleum Products Export Amounts of Refinery License Holders by years (ton) 40 Table Amounts of Products Offered to Domestic Market by the Refinery License Holders (1.000 tons)*** 41 Table Export Registered Deliveries by Refinery License Holders (ton) 42 Table Processing License Activities (unit) 42 Table Distribution License Activities (unit) 43 Table Amounts of Products Supplied from Refineries by Distribution License Holders (ton) 43 Table Liquid Fuels Purchased by Distribution License Holders within the Scope of Trade Between Distributors (ton)* 44 Table Sales within the Scope of Trade Between Distributors in Table Import Amounts of Distributor License Holders in 2012 by Fuel Type (ton) * 47 Table Import Amounts of Distributor License Holders in 2012 by Countries (ton) 48 Table Breakdown of Products Supplied by Distributor License Holders According to Sources (ton) 49 Table Fuel Sales Amounts of Distribution License Holders (ton) 50 Table Sectoral Breakdown of Liquid Fuel (excl. Bunker) Sales of Distribution License Holders in 2011 (%) 50 Table Sectoral Breakdown of Liquid Fuel (excl. Bunker) Sales of Distribution License Holders in 2012 (%) 50 Table Liquid Fuel and Autogas LPG Sales of Distribution License Holders by Fuel Types in (ton) 50 Table Fuel Oil Sales of Distribution License Holders in (ton) 51 Table Market Shares by Fuel Types* (ton) 51 Table Top 10 Distribution License Holders based on Sales 56 Table Breakdown of Monthly Liquid Fuel Sales of Distribution License Holders (ton) 57 Table Highest and Lowest Station Pump Sales in Table Breakdown of Fuel Types delivered to Fuel Vendors by License Holders (ton)* 59 Table Top 10 distribution license holders with highest figures of fuel delivery to vendor license holders, according to average delivery amounts per vendor 64

13 Table Average Daily Sales of Fuel Stations by Cities (Diesel and Gasoline Types Total) 66 Table Vendor License (Fuel)Holders Sales by Delivery Types (ton) 67 Table Top 20 Distribution License Holders According to Diesel and Gasoline Types Pump Sales by Their Vendors 67 Table Top 20 Distribution License Holders According to Tanker Sales for Agricultural Purpose and Village Pump Sales by Their Vendors 68 Table Top 20 Distribution License Holders According to Diesel and Gasoline Types Bulk Sales by Their Vendors 68 Table Fuel Sales through VIS by Distribution License Holders (ton) 69 Table Liquid Fuel Sales by Cities* (ton) 69 Table Station Pump Sales of Diesel Types by Cities (I) 76 Table Village Pump and Tanker Sales of Diesel Types for Agricultural Purposes by Cities (l) 79 Table Diesel Types Bulk Sales of Vendors by Cities (l) 82 Table Station Pump Sales of Gasoline Types by Cities (l) 85 Table Gasoline Types Bulk Sales of Vendors by Cities * (l) 88 Table Gasoil Sales of Vendors by Cities* (l) 91 Table Number of Stations Selling Unleaded Gasoline 95 Octane by Cities 95 Table Number of Stations Selling Diesel Fuel by Cities* 96 Table Distributor Sales to Eligible Users According to Fuel Types 97 Table Export Figures of Distribution License Holders by Fuel Types (ton)* 98 Table Bunker Delivery License Activities (Unit) 99 Table Bunker Delivery Activities in 2012 by Activity Types (Unit) 99 Table Bunker Delivery Subtitle Activities under Distribution Licenses 99 Table Import Figures of Distribution License Holders with Bunker Delivery Subtitle and Bunker Delivery License Holders (ton) 100 Table Procurement Figures of Distribution License Holders with Bunker Delivery Subtitle and Bunker Delivery License Holders (ton) 100 Table Marine Fuels sold in Domestic Market by Distribution License Holders with Bunker Delivery Subtitle and Bunker Delivery License Holders (ton) 101 Table Marine Fuels Exported in 2012 by Bunker Delivery License Holders and Distribution License Holders with Bunker Delivery Subtitle (ton) 105 Table Marine Fuels Delivered Subject to Transit Regime in 2012 by Bunker Delivery License Holders and Distribution License Holders with Bunker Delivery Subtitle (ton) 106 Table Aviation Fuels sold to Domestic Market by Distribution License Holders with Bunker Delivery Subtitle and Bunker Delivery License Holders (tons) 108 Table Aviation Fuels Exported in 2012 by Bunker Delivery License Holders and Distribution License Holders with Bunker Delivery Subtitle (ton) 109 Table Aviation Fuels Delivered Subject to Transit Regime in 2012 by Bunker Delivery License Holders and Distribution License Holders with Bunker Delivery Subtitle (ton) 110 Table Marine Fuels Delivered to Domestic Market between (with SCT and VAT) (tons)** 110 Table Marine Fuels Delivered to Domestic Market Between (SCT free with VAT) (ton) 112 Table Marine Fuels Exported Between (tons) 116 Table Marine Fuels Delivered Subject to Transit Regime Between (tons) 117 Table Aviation Fuels Delivered Domestically between (with SCT and VAT) (tons) 120 Table Aviation Fuels Exported Between (tons) 123 Table Aviation Fuels Delivered Subject to Transit Regime Between (tons) 124 Table Vendor License Activities (Unit) 126 Table Vendor License Activities in 2012 by Activity Types (Unit) 126 Table Vendor License Statistics 126 Table Number of Vendors of Distribution License Holders in Table Bunker Fuel Vendors with Stations by Cities by the end of

69 Table 2.")

14 Table Bunker Fuel Vendors without Stations by Cities by the end of Table Fuel Vendors with Stations by Cities by the end of Table 2.74 Fuel Vendors without Stations by Cities by the end of Table 2.75 Vendor Changes Between Distribution License Holders in Table Staff Numbers of Vendor License Holders by Cities According to their Distribution License Holders by the end of Table Eligible User License Activities (Unit) 143 Table Lubricant License Activities (Unit) 143 Table Lubricant Subtitle Activities under Distribution Licenses 143 Table Production Capacities of Lubricants License Holders (ton) * 143 Table Lubricant License Activities on Waste Oil Recovery 143 Table Lubricant Activities in 2012* 144 Table Storage License Activities (Unit) 144 Table Storage Licenses and Storage Capacities by the end of Table Storage Capacity for Providing Service to Third Parties (m 3 ) 149 Table Storage Subtitle License Activities under Distribution Licenses 149 Table Storage Capacity of the Distributor License Holders with Storage Subtitle by the end of 2010 (m³) 149 Table Storage Capacity of the Distributor License Holders with Storage Subtitle by the end of 2011 (m³) 149 Table Storage Capacity of the Distributor License Holders with Storage Subtitle by the end of 2012 (m³) 149 Table Storage Capacity of Refinery License Holders by the end of 2010 (m³)* 150 Table Storage Capacity of Refinery License Holders by the end of 2011 (m³)* 150 Table Storage Capacity of Refinery License Holders by the end of 2012 (m³)* 150 Table Warehouse Capacity of Refineries not active yet (m 3 ) 150 Table Transmission License Activities (Unit) 152 Table Transportation License Activities (Unit) 152 Table 3. 1 Brent (Dated) and Mediterranean Spot Prices (US Dollars) 154 Table Mediterranean Spot Prices and Average Import Prices of License Holders 155 Table 3. 3 Genova/Lavera CIF MED Average Price 157 Table 3. 4 Unleaded Gasoline 95 Octane Average Refinery Price 157 Table 3. 5 Unleaded Gasoline 95 Octane Distributor Depot Price 158 Table 3. 6 Unleaded Gasoline 95 Octane Vendor Prices 158 Table 3. 7 Unleaded Gasoline 95 Octane Monthly Average Price Formation ( /l) 158 Table 3. 8 Unleaded Gasoline 95 Octane Average Price 158 Table 3. 9 Shares of Tax and Sales Channels in Unleaded Gasoline 95 Octane Price (%) 161 Table Unleaded Gasoline 95 Octane (Other) Average Refinery price 162 Table Unleaded Gasoline 95 Octane (Other) Distributor Depot Price 162 Table Unleaded Gasoline 95 Octane (Other) Vendor Prices 162 Table Unleaded Gasoline 95 Octane (Other) Monthly Average Price Formation ( /l) 162 Table Unleaded Gasoline 95 Octane (Other) Average Price 163 Table Shares of Tax and Sales Channels in Unleaded Gasoline 95 Octane (Other) Price (%) 165 Table Diesel Average Refinery Price 166 Table Diesel Distributor Depot Price 166 Table Diesel Vendor Prices 166 Table Diesel Monthly Average Price Formation ( /l) 167 Table Diesel Average Price ( /l) 167 Table Shares of Tax and Sales Channels in Diesel Price (%) 170

143 Table 2. 79 Lubricant Subtitle Activities under Distribution Licenses 143 Table 2.")

15 Table Diesel (Other) Distributor Depot Price 171 Table Diesel (Other) Vendor Prices 171 Table Diesel (Other) Monthly Average Price Formation ( /l) 171 Table Diesel (Other) Average Price ( /l) 172 Table Shares of Tax and Sales Channels in Diesel (Other) Price (%) 174 Table Heating Oil (Sulphur level between 0.1% and 1%) Average Refinery Price 175 Table Heating Oil (Sulphur level between 0.1% and 1%) Distributor Depot Price 175 Table Heating Oil (Sulphur level between 0.1% and 1%) Vendor Price 175 Table Heating Oil (Sulphur level between 0.1% and 1%) Monthly Average Price Formation ( /kg) 176 Table Heating Oil (Sulphur level between 0.1% and 1%) Average Price 176 Table Shares of Tax and Sales Channels in Heating Oil Price (%) 179 Table High Sulphur Fuel Oil (Sulphur level above 1%) Average Refinery Price 180 Table High Sulphur Fuel Oil (Sulphur level above 1%) Distributor Depot Price 180 Table High Sulphur Fuel Oil (Sulphur level above 1%) Vendor Prices 180 Table High Sulphur Fuel Oil (Sulphur level above 1%) Monthly Average Price Formation ( /kg) 181 Table High Sulphur Fuel Oil (Sulphur level above 1%) Average Price 181 Table Shares of Tax and Sales Channels in High Sulphur Fuel Oil Price (%) 184 Table Indirect Taxes Collected from Liquid Fuel (billion ) 184 Table Amendments made in the sheets (A) and (B) of the list (I) of the SCT Law* 185 Table Average Vendor Price Changes in Selected EU countries 186 Table Storage Tariffs 189 Table Transmission Service Fees ( ) 191 Table 4. 1 Amounts of Liquid Fuel Marked with National Marker 193 Table 4. 2 Amounts of Ethanol and Biodiesel Marked with National Marker (m 3 ) 194 Table 4. 3 National Marker Field Device (XP) Measurements in Table 4. 4 Administrative Fines in Table 4. 5 Administrative Fines in Table 4. 6 Top 10 Cities in terms of Administrative Fines in the Petroleum Market between

Vendor Price 175 Table 3. 30 Heating Oil (Sulphur level between 0.1% and 1%) Monthly Average Price Formation ( /kg) 176 Table 3. 31 Heating Oil (Sulphur level between 0.")

16

17 LIST OF FIGURES Figure 1. 1 Breakdown of World Energy Consumption According to Primary Energy Sources 20 Figure 1. 2 Sectoral Breakdown of Petroleum Consumption 2009 Figures 21 Figure 1. 3 Sectoral Breakdown of Petroleum Consumption 2035 Projections 22 Figure 1. 4 Number of Refineries and Total Refining Capacity between Figure 2.1 Crude Oil procurement Amounts of Refinery License Holders Between (ton) 32 Figure 2.2 Amounts of Crude Oil Import from 6 Countries with the largest share 33 Figure 2.3 Breakdown of Crude Oil Imported by Refinery License Holders in 2012 According to Gravity (API) 34 Figure 2. 4 Import and Export of Intermediate Products by Refinery License Holders between Figure 2. 5 Percentages of Products Transformed from Crude Oil by Refinery License Holders in Figure 2. 6 Percentages of Products Transformed from Crude Oil by Refinery License Holders in Figure 2. 7 Monthly Diesel, Gasoline and Fuel Oil Production Figures of Refinery License Holders (1000 tons) 37 Figure 2. 8 Monthly Product Percentages Obtained from Crude Oil by Refineries in Turkey 38 Figure 2. 9 Petroleum Products Import Amounts of Refinery License Holders throughout Years 39 Figure Monthly Petroleum Products Export Amounts of Refinery License Holders in 2012 (1.000 tons) 40 Figure Petroleum Products Export Amounts of Refinery License Holders Throughout Years 41 Figure Breakdown of Monthly Liquid Fuel Delivery of Distribution License Holders 58 Figure Station Pump Sales 58 Figure Liquid Fuel Sales by Cities (ton) 72 Figure Liquid Fuel Sales by Regions 73 Figure Diesel Sales to Vendor License Holders by Cities (ton) 74 Figure Gasoline Sales to Vendor License Holders by Cities (ton) 75 Figure Market Concentrations of Fuel Sales (HHI) 98 Figure Marine Fuels Delivered to Domestic Market between (with SCT and VAT) (tons) 112 Figure Marine Fuels Delivered to Domestic Market Between (SCT free with VAT) (ton) 115 Figure Marine Fuels Exported Between (tons) 117 Figure Marine Fuels Delivered Subject to Transit Regime Between (tons) 120 Figure Amounts of Aviation Fuels Delivered Domestically between (with SCT and VAT) (tons) 122 Figure Aviation Fuels Exported Between (tons) 124 Figure Aviation Fuels Delivered Subject to Transit Regime Between (tons) 125 Figure Storage Capacities of Storage License Holders and Distribution License Holders with Storage Subtitle (m 3 ) 151 Figure 3. 1 Brent (Dated) and Mediterranean Spot Prices (US Dollars) 155 Figure 3. 2 Mediterranean Spot Prices and Turkey Prices ( /m 3 ) (Unleaded Gasoline 95 Octane) 156 Figure 3. 3 Mediterranean Spot Prices and Turkey Prices ( /m 3 ) (Diesel) 156 Figure 3. 4 Unleaded Gasoline 95 Octane Price Changes (without tax) ( /l) 160 Figure 3. 5 Unleaded Gasoline 95 Octane Price Changes (with tax) ( /l) 160 Figure 3. 6 Unleaded Gasoline 95 Octane Tax free Pump Price Formation ( /l) 161 Figure 3. 7 Shares of Tax and Sales Channels in Unleaded Gasoline 95 Octane Price 161 Figure 3. 8 Unleaded Gasoline 95 Octane (Other) Price Changes (without tax) ( /l) 164 Figure 3. 9 Unleaded Gasoline 95 Octane (Other) Price Changes (with tax) ( /l) 164 Figure Unleaded Gasoline 95 Octane (Other) Tax free Pump Price Formation ( /l) 165 Figure Shares of Tax and Sales Channels in Unleaded Gasoline 95 Octane (Other) Price 166

34 Figure 2.")

18 Figure Diesel Price Changes (without tax) ( /l) 168 Figure Diesel Price Changes (with tax)) ( /l) 169 Figure Diesel Tax free Pump Price Formation ( /l) 169 Figure Shares of Tax and Sales Channels in Diesel Price 170 Figure Diesel (other) Price Changes (without tax) ( /l) 173 Figure Diesel (other) Price Changes (with tax) ( /l) 173 Figure Diesel (Other) Tax free Pump Price Formation ( /l) 174 Figure Shares of Tax and Sales Channels in Diesel (Other) Price 175 Figure Heating Oil (Sulphur level between 0.1% and 1%) Price Changes (without tax) ( /kg) 178 Figure Heating Oil (Sulphur level between 0.1% and 1%) Price Changes (with tax) ( /kg) 178 Figure Heating Oil (Sulphur level between 0.1% and 1%) Tax free Pump Price Formation ( /kg) 179 Figure Shares of Tax and Sales Channels in Heating Oil Price 180 Figure High Sulphur Fuel Oil (Sulphur level above 1%) Price Changes (without tax) ( /kg) 182 Figure High Sulphur Fuel Oil (Sulphur level above 1%) Price Changes (with tax) ( /kg) ( /kg) 183 Figure High Sulphur Fuel Oil (Sulphur level above 1%) Tax free Pump Price Formation ( /kg) 183 Figure Shares of Tax and Sales Channels in High Sulphur Fuel Oil Price 184 Figure Indirect Tax Revenue from Liquid Fuels in 2012 (billion ) 185 Figure EU Vendor Price Changes (Without Tax) ( /l /kg) 187 Figure EU Vendor Price Changes (With Tax) ( /l /kg) 188 Figure Average Vendor Price Changes in Selected EU countries and Turkey ( /l) 118 Figure 4. 1 Amounts of Fuel Marked Between (million m 3 ) 194 Figure 4. 2 Breakdown of Fuel Marked by Distributors and Refineries 194 Figure 4. 3 Monthly Amounts of Fuel marked by Distributors and Refineries in 2011 (m 3 ) 195

Price Changes (without tax) ( /kg) 178 Figure 3. 21 Heating Oil (Sulphur level between 0.1% and 1%) Price Changes (with tax) ( /kg) 178 Figure 3. 22 Heating Oil (Sulphur level between 0.")

19 1. OIL IN THE WORLD In this section; world crude oil demand and supply, price flows and breakdown of refining capacities according to regions are analyzed under different headings.

20 1. OIL IN THE WORLD In this section; world crude oil demand and supply, price flows and breakdown of refining capacities according to regions are analyzed under different headings. Despite the opinion that oil will lose its significance among energy sources due to alternative energy sources and rapid depletion of oil reserves, oil continues to hold its key position as a strategic product as alternative energy sources are not yet economical enough and new reserves are discovered through new investments. Figure 1. 5 Breakdown of World Energy Consumption According to Primary Energy Sources Source: US Energy Information Administration, IEO2011&table=2 IEO2011®ion=0 0&cases=Reference 0504a_1630, February 2013 (Calculations based on figures in consumption table) 1.1 World Oil Demand World oil demand increased by 3.2% (2.72 million barrels per day) in 2010, by 0.7% (0.66 million barrels per day) in 2011 and by 1.3% (1.16 million barrels per day) in As a result, the average world oil demand reached 90 million barrels per day in Despite the fact that there is a relationship between oil consumption figures and the level of development of countries, Table 1.1, which displays oil consumption over the years, indicates that the total demand of developed OECD countries was 51.3% and the total demand of non OECD countries was 48.7% in 2012 without a significant change compared to the previous year. In 2012, while there was an increase of 0.4 million barrels per day in the demand of non OECD nations, the demand of OECD nations increased by 0.5 million barrels per day and the net increase in world demand totaled 0.9 million barrels per day.

PETROLEUM MARKET SECTOR REPORT PETROLEUM MARKET DEPARTMENT MARCH

PETROLEUM MARKET SECTOR REPORT PETROLEUM MARKET DEPARTMENT MARCH TABLES Table 1 2012 Mart Ayı Dağıtıcı ve İhrakiye Teslimi Lisansı Sahiplerinin Petrol İthalatı Table 2 2012 Mart Ayı Rafinerici Lisansı

PETROLEUM MARKET SECTOR REPORT PETROLEUM MARKET DEPARTMENT MARCH TABLES Table 1 2012 Mart Ayı Dağıtıcı ve İhrakiye Teslimi Lisansı Sahiplerinin Petrol İthalatı Table 2 2012 Mart Ayı Rafinerici Lisansı

T.C. SÜLEYMAN DEMİREL ÜNİVERSİTESİ FEN BİLİMLERİ ENSTİTÜSÜ ISPARTA İLİ KİRAZ İHRACATININ ANALİZİ

T.C. SÜLEYMAN DEMİREL ÜNİVERSİTESİ FEN BİLİMLERİ ENSTİTÜSÜ ISPARTA İLİ KİRAZ İHRACATININ ANALİZİ Danışman Doç. Dr. Tufan BAL YÜKSEK LİSANS TEZİ TARIM EKONOMİSİ ANABİLİM DALI ISPARTA - 2016 2016 [] TEZ

T.C. SÜLEYMAN DEMİREL ÜNİVERSİTESİ FEN BİLİMLERİ ENSTİTÜSÜ ISPARTA İLİ KİRAZ İHRACATININ ANALİZİ Danışman Doç. Dr. Tufan BAL YÜKSEK LİSANS TEZİ TARIM EKONOMİSİ ANABİLİM DALI ISPARTA - 2016 2016 [] TEZ

TÜRKİYE PLASTİK SEKTÖR PROFİLİ 2013 İtibariyle

PROSES KAPASİTESİ ( BİTMİŞ MAMUL ÜRETİMİ ) TÜRKİYE PLASTİK SEKTÖR PROFİLİ 2013 İtibariyle 8,1 Milyon Ton BİTMİŞ MAMUL ÜRETİM DEĞERİ 34 Milyar $ EKONOMİYE SAĞLANAN KATMA DEĞER 13 Milyar $ SEKTÖRÜN PROSES

PROSES KAPASİTESİ ( BİTMİŞ MAMUL ÜRETİMİ ) TÜRKİYE PLASTİK SEKTÖR PROFİLİ 2013 İtibariyle 8,1 Milyon Ton BİTMİŞ MAMUL ÜRETİM DEĞERİ 34 Milyar $ EKONOMİYE SAĞLANAN KATMA DEĞER 13 Milyar $ SEKTÖRÜN PROSES

ISSN: Yıl /Year: 2017 Cilt(Sayı)/Vol.(Issue): 1(Özel) Sayfa/Page: Araştırma Makalesi Research Article

/Vol.(Issue): 1(Özel) Sayfa/Page: Araştırma Makalesi Research Article") VII. Bahçe Ürünlerinde Muhafaza ve Pazarlama Sempozyumu, 04-07 Ekim 2016 ISSN: 2148-0036 Yıl /Year: 2017 Cilt(Sayı)/Vol.(Issue): 1(Özel) Sayfa/Page: 173-180 Araştırma Makalesi Research Article Akdeniz

VII. Bahçe Ürünlerinde Muhafaza ve Pazarlama Sempozyumu, 04-07 Ekim 2016 ISSN: 2148-0036 Yıl /Year: 2017 Cilt(Sayı)/Vol.(Issue): 1(Özel) Sayfa/Page: 173-180 Araştırma Makalesi Research Article Akdeniz

HAKKIMIZDA ABOUT US. kuruluşundan bugüne PVC granül sektöründe küresel ve etkin bir oyuncu olmaktır.

ABOUT US HAKKIMIZDA FORPLAS ın temel amacı, kuruluşundan bugüne PVC granül sektöründe küresel ve etkin bir oyuncu olmaktır. 25 yılı aşkın üretim deneyimine sahip olan FORPLAS, geniş ve nitelikli ürün yelpazesiyle

ABOUT US HAKKIMIZDA FORPLAS ın temel amacı, kuruluşundan bugüne PVC granül sektöründe küresel ve etkin bir oyuncu olmaktır. 25 yılı aşkın üretim deneyimine sahip olan FORPLAS, geniş ve nitelikli ürün yelpazesiyle

Quarterly Statistics by Banks, Employees and Branches in Banking System

Quarterly Statistics by Banks, Employees and Branches in Banking System March 2018 Report Code: DE13 April 2018 Contents Page No. Number of Banks... Number of Employees. Bank Employees by Gender and Education

Quarterly Statistics by Banks, Employees and Branches in Banking System March 2018 Report Code: DE13 April 2018 Contents Page No. Number of Banks... Number of Employees. Bank Employees by Gender and Education

Inventory of LCPs in Turkey LCP Database explained and explored

Inventory of LCPs in Turkey LCP Database explained and explored Hakan Hatipoglu Antalya, 9 October 2015 Requirements and specifications (TOR) Web based database application that will: Support Inventory

Inventory of LCPs in Turkey LCP Database explained and explored Hakan Hatipoglu Antalya, 9 October 2015 Requirements and specifications (TOR) Web based database application that will: Support Inventory

EPPAM BÜLTENİ. İstanbul Aydın Üniversitesi EPPAM Yıl 2, Sayı 7, Temmuz 2017

EPPAM BÜLTENİ İstanbul Aydın Üniversitesi EPPAM DIŞ EKONOMİK İLİŞKİLER KURULU-DEİK ENERJİ İŞ KONSEYİ TEMMUZ TOPLANTISI İçindekiler DEİK Enerji İş Konseyi 1 Sahra Altı Afrika Enerji Yatırım 2 Uluslararası

EPPAM BÜLTENİ İstanbul Aydın Üniversitesi EPPAM DIŞ EKONOMİK İLİŞKİLER KURULU-DEİK ENERJİ İŞ KONSEYİ TEMMUZ TOPLANTISI İçindekiler DEİK Enerji İş Konseyi 1 Sahra Altı Afrika Enerji Yatırım 2 Uluslararası

A.Ş. ÖZEL / FASON ÜRETİM

ÖZEL / FASON ÜRETİM Private Label www.jeomed.com Private / Contract Manufacturing How is it performed? 01 New Products Market Research 02 Product R & D 03 Ministry of Health Operations 04 GMP Norms Production

ÖZEL / FASON ÜRETİM Private Label www.jeomed.com Private / Contract Manufacturing How is it performed? 01 New Products Market Research 02 Product R & D 03 Ministry of Health Operations 04 GMP Norms Production

THE DESIGN AND USE OF CONTINUOUS GNSS REFERENCE NETWORKS. by Özgür Avcı B.S., Istanbul Technical University, 2003

THE DESIGN AND USE OF CONTINUOUS GNSS REFERENCE NETWORKS by Özgür Avcı B.S., Istanbul Technical University, 2003 Submitted to the Kandilli Observatory and Earthquake Research Institute in partial fulfillment

THE DESIGN AND USE OF CONTINUOUS GNSS REFERENCE NETWORKS by Özgür Avcı B.S., Istanbul Technical University, 2003 Submitted to the Kandilli Observatory and Earthquake Research Institute in partial fulfillment

Turkish Vessel Monitoring System. Turkish VMS

Turkish Vessel Monitoring System BSGM Balıkçılık ve Su Ürünleri Genel Balıkçılık Müdürlüğü ve Su Ürünleri Genel Müdürlüğü İstatistik ve Bilgi Sistemleri İstatistik Daire Başkanlığı ve Bilgi Sistemleri

Turkish Vessel Monitoring System BSGM Balıkçılık ve Su Ürünleri Genel Balıkçılık Müdürlüğü ve Su Ürünleri Genel Müdürlüğü İstatistik ve Bilgi Sistemleri İstatistik Daire Başkanlığı ve Bilgi Sistemleri

EPPAM BÜLTENİ. İstanbul Aydın Üniversitesi EPPAM Yıl 2, Sayı 4, Nisan 2017

EPPAM BÜLTENİ İstanbul Aydın Üniversitesi EPPAM ENERJİ GÜVENLİĞİ ULUSLARARASI PROJESİ İçindekiler Enerji Güvenliği Projesi 1 Çevre Güvenliği Kitabı 2 Karadeniz de Bölgesel İşbirliği Kon. 2 EPPAM Basın

EPPAM BÜLTENİ İstanbul Aydın Üniversitesi EPPAM ENERJİ GÜVENLİĞİ ULUSLARARASI PROJESİ İçindekiler Enerji Güvenliği Projesi 1 Çevre Güvenliği Kitabı 2 Karadeniz de Bölgesel İşbirliği Kon. 2 EPPAM Basın

Dünya ve 20 Gelişmiş Ülke Ekonomisinde Hayvancılığın Yeri

1 2 3 Dünya ve 20 Gelişmiş Ülke Ekonomisinde Hayvancılığın Yeri Özet Dünyada kişi başına düşen günlük hayvansal protein miktarı 1961 ve 2011 yıllarında sırasıyla 19,7 ve 31,8 gramdır. Bu miktarlar 1961

1 2 3 Dünya ve 20 Gelişmiş Ülke Ekonomisinde Hayvancılığın Yeri Özet Dünyada kişi başına düşen günlük hayvansal protein miktarı 1961 ve 2011 yıllarında sırasıyla 19,7 ve 31,8 gramdır. Bu miktarlar 1961

FISHERIES and AQUACULTURE in TURKEY

FISHERIES and AQUACULTURE in TURKEY The Regional Workshop The World Trade Organisation (WTO) and Fisheries St. Petersburg, 29 31 October 2013 Binnur CEYLAN (MSc) Erdal USTUNDAG (PhD) Department of Aquaculture

FISHERIES and AQUACULTURE in TURKEY The Regional Workshop The World Trade Organisation (WTO) and Fisheries St. Petersburg, 29 31 October 2013 Binnur CEYLAN (MSc) Erdal USTUNDAG (PhD) Department of Aquaculture

BPR NİN ETKİLERİ. Selim ATAK Çevre Mühendisi Environmental Engineer

BPR NİN ETKİLERİ Impacts of the BPR Selim ATAK Çevre Mühendisi Environmental Engineer 98/8/EC sayılı Biyosidal Ürünlerin Piyasaya Arzına İlişkin Avrupa Parlamentosu ve Konseyi Direktifi, Avrupa Birliği

BPR NİN ETKİLERİ Impacts of the BPR Selim ATAK Çevre Mühendisi Environmental Engineer 98/8/EC sayılı Biyosidal Ürünlerin Piyasaya Arzına İlişkin Avrupa Parlamentosu ve Konseyi Direktifi, Avrupa Birliği

Effect of Crude Oil Price in Turkey and GYP

Effect of Crude Oil Price in Turkey and GYP Fatih Güler General Manager 26. ITU Petrol ve Doğal Gaz Seminer ve Sergisi 23 24 Haziran 2016 ISTANBUL CONTENTS Fall in Oil Prices Effect of Oil Pi Price reduction

Effect of Crude Oil Price in Turkey and GYP Fatih Güler General Manager 26. ITU Petrol ve Doğal Gaz Seminer ve Sergisi 23 24 Haziran 2016 ISTANBUL CONTENTS Fall in Oil Prices Effect of Oil Pi Price reduction

ISSN: Yıl /Year: 2017 Cilt(Sayı)/Vol.(Issue): 1(Özel) Sayfa/Page: Araştırma Makalesi Research Article. Özet.

/Vol.(Issue): 1(Özel) Sayfa/Page: Araştırma Makalesi Research Article. Özet.") VII. Bahçe Ürünlerinde Muhafaza ve Pazarlama Sempozyumu, 04-07 Ekim 206 ISSN: 248-0036 Yıl /Year: 207 Cilt(Sayı)/Vol.(Issue): (Özel) Sayfa/Page: 54-60 Araştırma Makalesi Research Article Suleyman Demirel

VII. Bahçe Ürünlerinde Muhafaza ve Pazarlama Sempozyumu, 04-07 Ekim 206 ISSN: 248-0036 Yıl /Year: 207 Cilt(Sayı)/Vol.(Issue): (Özel) Sayfa/Page: 54-60 Araştırma Makalesi Research Article Suleyman Demirel

WATER AND IRRIGATION SECTOR IN TURKEY

WATER AND IRRIGATION SECTOR IN TURKEY ZARAGOZA, 7th March 2017 FATMA KAYHAN COMMERCIAL COUNSELOR Oficina Comercial de la Embajada de Turquía en Madrid Embassy of the Republic of Turkey-Commercial Office

WATER AND IRRIGATION SECTOR IN TURKEY ZARAGOZA, 7th March 2017 FATMA KAYHAN COMMERCIAL COUNSELOR Oficina Comercial de la Embajada de Turquía en Madrid Embassy of the Republic of Turkey-Commercial Office

B a n. Quarterly Statistics by Banks, Employees and Branches in Banking System. Report Code: DE13 July 2018

B a n Quarterly Statistics by Banks, Employees and Branches in Banking System H June 2018 T Report Code: DE13 July 2018 Contents Page No. Number of Banks... Number of Employees. Bank Employees by Gender

B a n Quarterly Statistics by Banks, Employees and Branches in Banking System H June 2018 T Report Code: DE13 July 2018 Contents Page No. Number of Banks... Number of Employees. Bank Employees by Gender

PETDER OPINION ON EMRA BOARD DECISION ON CEILING PRICE IMPLEMENTATION

February 2015 PETDER plants one tree for each barrel of waste engine oil collected within the framework of One Barrel One Tree Project carried out under the protocol signed with Ministry of Environment

February 2015 PETDER plants one tree for each barrel of waste engine oil collected within the framework of One Barrel One Tree Project carried out under the protocol signed with Ministry of Environment

Erol KAYA Yönetim Kurulu Başkanı Chairman Of The Board

Arifiye Fidancılık 1989 yılında Adapazarı Arifiye ilçesinde kurulmuştur. Kuruluşumuz 300 m2 alanda mevsimlik çiçek üretimi ve satışı ile faaliyet göstermeye başlamıştır. Geçen süre içersinde marka haline

Arifiye Fidancılık 1989 yılında Adapazarı Arifiye ilçesinde kurulmuştur. Kuruluşumuz 300 m2 alanda mevsimlik çiçek üretimi ve satışı ile faaliyet göstermeye başlamıştır. Geçen süre içersinde marka haline

First Stage of an Automated Content-Based Citation Analysis Study: Detection of Citation Sentences

First Stage of an Automated Content-Based Citation Analysis Study: Detection of Citation Sentences Zehra Taşkın, Umut Al & Umut Sezen {ztaskin, umutal, u.sezen}@hacettepe.edu.tr - 1 Plan Need for content-based

First Stage of an Automated Content-Based Citation Analysis Study: Detection of Citation Sentences Zehra Taşkın, Umut Al & Umut Sezen {ztaskin, umutal, u.sezen}@hacettepe.edu.tr - 1 Plan Need for content-based

Vakko Tekstil ve Hazir Giyim Sanayi Isletmeleri A.S. Company Profile- Outlook, Business Segments, Competitors, Goods and Services, SWOT and Financial

Vakko Tekstil ve Hazir Giyim Sanayi Isletmeleri A.S. Company Profile- Outlook, Business Segments, Competitors, Goods and Services, SWOT and Financial Analysis Vakko Tekstil ve Hazir Giyim Sanayi Isletmeleri

Vakko Tekstil ve Hazir Giyim Sanayi Isletmeleri A.S. Company Profile- Outlook, Business Segments, Competitors, Goods and Services, SWOT and Financial Analysis Vakko Tekstil ve Hazir Giyim Sanayi Isletmeleri

Yüz Tanımaya Dayalı Uygulamalar. (Özet)

") 4 Yüz Tanımaya Dayalı Uygulamalar (Özet) Günümüzde, teknolojinin gelişmesi ile yüz tanımaya dayalı bir çok yöntem artık uygulama alanı bulabilmekte ve gittikçe de önem kazanmaktadır. Bir çok farklı uygulama

4 Yüz Tanımaya Dayalı Uygulamalar (Özet) Günümüzde, teknolojinin gelişmesi ile yüz tanımaya dayalı bir çok yöntem artık uygulama alanı bulabilmekte ve gittikçe de önem kazanmaktadır. Bir çok farklı uygulama

04 www.borpanel.com.tr

BANYO MOBiLYALARI 04 Kalite Yönetim Modern yaşamın koşuşturmasında Belgeleri klasikten vazgeçemeyenlere konfor ve estetiği bir arada sunan Efes, banyolarınızın atmosferini değiştirecek. 05 06 KURUMSAL

BANYO MOBiLYALARI 04 Kalite Yönetim Modern yaşamın koşuşturmasında Belgeleri klasikten vazgeçemeyenlere konfor ve estetiği bir arada sunan Efes, banyolarınızın atmosferini değiştirecek. 05 06 KURUMSAL

HAZIRLAYANLAR: K. ALBAYRAK, E. CİĞEROĞLU, M. İ. GÖKLER

HAZIRLAYANLAR: K. ALBAYRAK, E. CİĞEROĞLU, M. İ. GÖKLER PROGRAM OUTCOME 13 Ability to Take Societal, Environmental and Economical Considerations into Account in Professional Activities Program outcome 13

HAZIRLAYANLAR: K. ALBAYRAK, E. CİĞEROĞLU, M. İ. GÖKLER PROGRAM OUTCOME 13 Ability to Take Societal, Environmental and Economical Considerations into Account in Professional Activities Program outcome 13

YIL ÜRETİM ALANI(da) ÜRETİM(ton)

ÜRETİM(ton)") DÜNYA ŞARAP ÜRETİMİ Son 15 yılda 2 kat büyüyen dünya şarap ticaretinde, ihracat miktarı açısından üçüncü olmasına rağmen, 8.3 milyar dolarlık gelirle zirvede bulunan Fransa, şarapçılıktaki gelirlerini

DÜNYA ŞARAP ÜRETİMİ Son 15 yılda 2 kat büyüyen dünya şarap ticaretinde, ihracat miktarı açısından üçüncü olmasına rağmen, 8.3 milyar dolarlık gelirle zirvede bulunan Fransa, şarapçılıktaki gelirlerini

Experiences with Self Consumption Projects

Experiences with Self Consumption Projects Özgür SARPDAĞ Business Development Manager 9 th of April, Wednesday Solarpraxis PV Power Plants Turkey New Energy Renewable Energy Index 1. ELSE Enerji References

Experiences with Self Consumption Projects Özgür SARPDAĞ Business Development Manager 9 th of April, Wednesday Solarpraxis PV Power Plants Turkey New Energy Renewable Energy Index 1. ELSE Enerji References

ORGANIC FARMING IN TURKEY

Republic of Turkey Ministry of Food Agriculture and Livestock General Directorate of Plant Production ORGANIC FARMING IN TURKEY By Vildan KARAARSLAN Head of Department Agronomist and Food Science Expert

Republic of Turkey Ministry of Food Agriculture and Livestock General Directorate of Plant Production ORGANIC FARMING IN TURKEY By Vildan KARAARSLAN Head of Department Agronomist and Food Science Expert

Mehmet MARANGOZ * ** *** stratejileri ve ekonomik yenilikleri ile. ecindeki. alternatif g. Anahtar Kelimeler:

Mehmet MARANGOZ * ** *** stratejileri ve ekonomik yenilikleri ile ecindeki alternatif g e Anahtar Kelimeler: ENTREPRENEUR CITY GAZIANTEP AND BORDER TRADE ABSTRACT A society's economic, political and cultural

Mehmet MARANGOZ * ** *** stratejileri ve ekonomik yenilikleri ile ecindeki alternatif g e Anahtar Kelimeler: ENTREPRENEUR CITY GAZIANTEP AND BORDER TRADE ABSTRACT A society's economic, political and cultural

Bilim ve Teknoloji Science and Technology

19 Bilim ve Teknoloji Bilim ve Teknoloji 19.1 Hanelerde bilişim teknolojileri bulunma ve İnternete bağlılık oranı,2017 Proportion of information and communication technology devices in households and its

19 Bilim ve Teknoloji Bilim ve Teknoloji 19.1 Hanelerde bilişim teknolojileri bulunma ve İnternete bağlılık oranı,2017 Proportion of information and communication technology devices in households and its

Unlike analytical solutions, numerical methods have an error range. In addition to this

ERROR Unlike analytical solutions, numerical methods have an error range. In addition to this input data may have errors. There are 5 basis source of error: The Source of Error 1. Measuring Errors Data

ERROR Unlike analytical solutions, numerical methods have an error range. In addition to this input data may have errors. There are 5 basis source of error: The Source of Error 1. Measuring Errors Data

PRODUCT CATALOGUE ÜRÜN KATALOĞU

PRODUCT CATALOGUE ÜRÜN KATALOĞU 2019 www.basakdeterjan.com info@basakdeterjan.com HAKKIMIZDA / ABOUT US BSK Grup 1989 yilindan itibaren deterjan, temizlik urunleri ve kozmetik sektörünün içinde olan 2000

PRODUCT CATALOGUE ÜRÜN KATALOĞU 2019 www.basakdeterjan.com info@basakdeterjan.com HAKKIMIZDA / ABOUT US BSK Grup 1989 yilindan itibaren deterjan, temizlik urunleri ve kozmetik sektörünün içinde olan 2000

AKIS continues manufacturing the products with an integrated system in its facilities which are located in Konya Organized

HAKKIMIZDA Üretim hayatına 1978 yılında başlayan AKIŞ, zaman içerisinde elde ettiği deneyim ve bilgiyi, yeni teknoloji yatırımları ile buluşturarak, Asansör sektörünün ülkemizdeki ve dünyadaki önemli temsilcilerinden

HAKKIMIZDA Üretim hayatına 1978 yılında başlayan AKIŞ, zaman içerisinde elde ettiği deneyim ve bilgiyi, yeni teknoloji yatırımları ile buluşturarak, Asansör sektörünün ülkemizdeki ve dünyadaki önemli temsilcilerinden

Draft CMB Legislation Prospectus Directive

Draft CMB Legislation Prospectus Directive Ayşegül Ekşit, SPK / CMB 1 Kapsam İzahname Konulu Taslaklar İzahname Yayınlama Zorunluluğu ve Muafiyetler İzahnamenin Onay Süreci İzahname Standartları İzahnamenin

Draft CMB Legislation Prospectus Directive Ayşegül Ekşit, SPK / CMB 1 Kapsam İzahname Konulu Taslaklar İzahname Yayınlama Zorunluluğu ve Muafiyetler İzahnamenin Onay Süreci İzahname Standartları İzahnamenin

Electricity Generated From Coal. Coal Based Generation: in 2008: 41% in 2030: 44%

Electricity Generated From Coal Billion kwh 16000 14000 12000 10000 8000 6000 WORLD 1973: 6118 Billion kwh 2008: 20269 Billion kwh 2030: 33252 Billion kwh 4000 2000 0 Coal Gas Nuclear Hydro Oil Bio and

Electricity Generated From Coal Billion kwh 16000 14000 12000 10000 8000 6000 WORLD 1973: 6118 Billion kwh 2008: 20269 Billion kwh 2030: 33252 Billion kwh 4000 2000 0 Coal Gas Nuclear Hydro Oil Bio and

«Live 0Emisson» Christoph M. Grosser. Friedrichshafen, 27.08.2014. 0 emisyon Enerji ve Teknoloji Sanayi ve Ticaret A.Ş.

«Live 0Emisson» Christoph M. Grosser Friedrichshafen, 27.08.2014 Agenda Personal presentation Brief information about Turkey 0 emisyon A.Ş. (AG) Vision und Strategy Brief information about the Turkish

«Live 0Emisson» Christoph M. Grosser Friedrichshafen, 27.08.2014 Agenda Personal presentation Brief information about Turkey 0 emisyon A.Ş. (AG) Vision und Strategy Brief information about the Turkish

Quarterly Statistics by Banks, Employees and Branches in Banking

Quarterly Statistics by Banks, Employees and Branches in Banking E September 2018 E Report Code: DE13 November 2018 Contents Page No. Number of Banks... Number of Employees. Bank Employees by Gender and

Quarterly Statistics by Banks, Employees and Branches in Banking E September 2018 E Report Code: DE13 November 2018 Contents Page No. Number of Banks... Number of Employees. Bank Employees by Gender and

NOVAPAC Ambalaj San. Tic. A.Ş

Ambalaj San. Tic. A.Ş 2014 yılında İstanbul'da 5.000 m2 lik alanda kurulan tek kullanımlık plastik ürünleri araştırıp, geliştirip, tasarlayıp üretmektedir. Uzun yılların deneyimi ile pazara yenilikçi,

Ambalaj San. Tic. A.Ş 2014 yılında İstanbul'da 5.000 m2 lik alanda kurulan tek kullanımlık plastik ürünleri araştırıp, geliştirip, tasarlayıp üretmektedir. Uzun yılların deneyimi ile pazara yenilikçi,

Firma Profili 1970 yılında Mehmet Ali Atiker tarafından çelik sacdan sondaj teçhiz boruları üretmek üzere kurulmuş küçük bir işletme iken zaman içerisinde gelişerek büyüyen Atiker Metal A.Ş. üretim konusunu

Firma Profili 1970 yılında Mehmet Ali Atiker tarafından çelik sacdan sondaj teçhiz boruları üretmek üzere kurulmuş küçük bir işletme iken zaman içerisinde gelişerek büyüyen Atiker Metal A.Ş. üretim konusunu

www.yorukhidrolik.com www.bombe.gen.tr BİZ KİMİZ? WHO ARE WE? Firmamız hidrolik pres konusunda Türk sanayisine hizmet etmek için 1980 yılında şahıs firması olarak kurulmuştur. Hidrolik Pres imalatına o

www.yorukhidrolik.com www.bombe.gen.tr BİZ KİMİZ? WHO ARE WE? Firmamız hidrolik pres konusunda Türk sanayisine hizmet etmek için 1980 yılında şahıs firması olarak kurulmuştur. Hidrolik Pres imalatına o

Republic of Turkey Ministry of Finance General Directorate of National Immovables Performance Agreement

Republic of Turkey Ministry of Finance General Directorate of National Immovables Performance Agreement Presentation Plan Possible Amendments Strategic Policies Performance Targets Activities Operational

Republic of Turkey Ministry of Finance General Directorate of National Immovables Performance Agreement Presentation Plan Possible Amendments Strategic Policies Performance Targets Activities Operational

Network Principles, Tariffs, International Integration and Re- Export Opportunities. H. Hakan ÜNAL (M.Sc.) Dr. iur. Cafer EMİNOĞLU

Dr. iur. Cafer EMİNOĞLU") BOTAŞ TURKEY Network Principles, Tariffs, International Integration and Re- Export Opportunities H. Hakan ÜNAL (M.Sc.) Dr. iur. Cafer EMİNOĞLU BOTAŞ Gas Transmission Management European Gas Conference

BOTAŞ TURKEY Network Principles, Tariffs, International Integration and Re- Export Opportunities H. Hakan ÜNAL (M.Sc.) Dr. iur. Cafer EMİNOĞLU BOTAŞ Gas Transmission Management European Gas Conference

ÖNEMLİ DUYURU İTKİB GENEL SEKRETERLİĞİ

ÖNEMLİ DUYURU Sayın Yetkili/İlgili; Bilindiği üzere, 2010/1 sayılı İthalatta Gözetim Uygulanmasına İlişkin Tebliğ kapsamında bahse konu tebliğin ekinde fasıl ve gümrük tarife pozisyonu belirtilen eşyanın

ÖNEMLİ DUYURU Sayın Yetkili/İlgili; Bilindiği üzere, 2010/1 sayılı İthalatta Gözetim Uygulanmasına İlişkin Tebliğ kapsamında bahse konu tebliğin ekinde fasıl ve gümrük tarife pozisyonu belirtilen eşyanın

Ulaştırma ve Haberleşme Transportation and Communication

16 Ulaştırma ve Haberleşme Ulaştırma ve Haberleşme 16.1 Otoyol, devlet, il ve köy yolları uzunluğu, 2015-2017 Length of motorways, state highways, provincial roads and village roads, 2015-2017 (Km) Otoyol-Motorways

16 Ulaştırma ve Haberleşme Ulaştırma ve Haberleşme 16.1 Otoyol, devlet, il ve köy yolları uzunluğu, 2015-2017 Length of motorways, state highways, provincial roads and village roads, 2015-2017 (Km) Otoyol-Motorways

Deri ve Deri Konfeksiyon Fuarı Leather and Leather Garment Fair İZMİR / TURKEY. leatherandmore.izfas.com.tr

Deri ve Deri Konfeksiyon Fuarı İZMİR / TURKEY leatherandmore.izfas.com.tr LEATHER & MORE İzmir Büyükşehir Belediyesi ev sahipliğinde İZFAŞ tarafından organize edilecek olan Leather & More Deri ve Deri

Deri ve Deri Konfeksiyon Fuarı İZMİR / TURKEY leatherandmore.izfas.com.tr LEATHER & MORE İzmir Büyükşehir Belediyesi ev sahipliğinde İZFAŞ tarafından organize edilecek olan Leather & More Deri ve Deri

Tanrıkulu şirketler grubu kâğıt metal ve plastik olmak üzere üç ana dalda, İstanbul, Kocaeli ve Sakarya gibi üç büyük şehirde 1989 yılından beri

Tanrıkulu şirketler grubu kâğıt metal ve plastik olmak üzere üç ana dalda, İstanbul, Kocaeli ve Sakarya gibi üç büyük şehirde 1989 yılından beri geridönüşüm faaliyetlerini sürdürmektedir. Tanrıkulu Plastik

Tanrıkulu şirketler grubu kâğıt metal ve plastik olmak üzere üç ana dalda, İstanbul, Kocaeli ve Sakarya gibi üç büyük şehirde 1989 yılından beri geridönüşüm faaliyetlerini sürdürmektedir. Tanrıkulu Plastik

Privatization of Water Distribution and Sewerages Systems in Istanbul Assoc. Prof. Dr. Eyup DEBIK Menekse Koral Isik

Privatization of Water Distribution and Sewerages Systems in Istanbul Assoc. Prof. Dr. Eyup DEBIK Menekse Koral Isik Yildiz Technical University, Environmental Engineering Dept., Istanbul-Turkey Aim and

Privatization of Water Distribution and Sewerages Systems in Istanbul Assoc. Prof. Dr. Eyup DEBIK Menekse Koral Isik Yildiz Technical University, Environmental Engineering Dept., Istanbul-Turkey Aim and

AKDENİZ ÜNİVERSİTESİ MÜHENDİSLİK FAKÜLTESİ ÇEVRE MÜHENDİSLİĞİ BÖLÜMÜ ÇEV181 TEKNİK İNGİLİZCE I

AKDENİZ ÜNİVERSİTESİ MÜHENDİSLİK FAKÜLTESİ ÇEVRE MÜHENDİSLİĞİ BÖLÜMÜ ÇEV181 TEKNİK İNGİLİZCE I Dr. Öğr. Üyesi Firdes YENİLMEZ KTS Kredisi 3 (Kurumsal Saat: 2 Uygulama Saat: 1) Ders Programı Pazartesi 09:30-12:20

AKDENİZ ÜNİVERSİTESİ MÜHENDİSLİK FAKÜLTESİ ÇEVRE MÜHENDİSLİĞİ BÖLÜMÜ ÇEV181 TEKNİK İNGİLİZCE I Dr. Öğr. Üyesi Firdes YENİLMEZ KTS Kredisi 3 (Kurumsal Saat: 2 Uygulama Saat: 1) Ders Programı Pazartesi 09:30-12:20

S u G e ç i r m e z.

Hakkımızda Otomotiv aydınlatma sektöründe geçirilen 5 yıllık tecrübenin birikimi ile kurulan ThocAUTO, kurulduğu günden bu yana izlemiş olduğu yenilikçi stratejiler ve müşteri odaklı satış politikası sayesinde

Hakkımızda Otomotiv aydınlatma sektöründe geçirilen 5 yıllık tecrübenin birikimi ile kurulan ThocAUTO, kurulduğu günden bu yana izlemiş olduğu yenilikçi stratejiler ve müşteri odaklı satış politikası sayesinde

Enerjide Çözüm: Enerjinin Etkin Kullanımı ve %100 Yenilenebilir Enerji

Enerjide Çözüm: Enerjinin Etkin Kullanımı ve %100 Yenilenebilir Enerji Prof. Dr. Tanay Sıdkı UYAR, Öğretim Üyesi EUROSOLAR Avrupa Yenilenebilir Enerji Birliği Başkan Yardımcısı WWEA Dünya Rüzgar Enerjisi

Enerjide Çözüm: Enerjinin Etkin Kullanımı ve %100 Yenilenebilir Enerji Prof. Dr. Tanay Sıdkı UYAR, Öğretim Üyesi EUROSOLAR Avrupa Yenilenebilir Enerji Birliği Başkan Yardımcısı WWEA Dünya Rüzgar Enerjisi

Tuğra Makina bu katalogtaki tüm bilgiler üzerinde değișiklik yapma hakkı saklıdır. Tugra Makina all rights reserved to change all information in this

Tuğra Makina bu katalogtaki tüm bilgiler üzerinde değișiklik yapma hakkı saklıdır. Tugra Makina all rights reserved to change all information in this catalog. 1997 yılında muhtelif metal eșya, sac metal,

Tuğra Makina bu katalogtaki tüm bilgiler üzerinde değișiklik yapma hakkı saklıdır. Tugra Makina all rights reserved to change all information in this catalog. 1997 yılında muhtelif metal eșya, sac metal,

M mar S stemler Arch tectural Systems

M mar S stemler Arch tectural Systems 1974 yılından itibaren Türkiye de alüminyum profil sektöründe faaliyet göstermekte olan Astaş Alüminyum San. ve Tic. AŞ sektörün öncü ve lider firmalarından birisidir.

M mar S stemler Arch tectural Systems 1974 yılından itibaren Türkiye de alüminyum profil sektöründe faaliyet göstermekte olan Astaş Alüminyum San. ve Tic. AŞ sektörün öncü ve lider firmalarından birisidir.

C O N T E N T S BHD BHD page 2-5 BHD page 6-9 BHD page BHD page page BHD

C O N T E N T S BHD 32 + 4 BHD 28 + 4 BHD 24 + 3 page 2-5 page 6-9 BHD 19 + 3 page 10-13 BHD 18 + 3 page 14-17 BHD 18 + 3 page 18-21 BHD 17 + 3 page 18-21 BHDM 12 + 3 page 22-25 page 26-28 Boom Makina;

C O N T E N T S BHD 32 + 4 BHD 28 + 4 BHD 24 + 3 page 2-5 page 6-9 BHD 19 + 3 page 10-13 BHD 18 + 3 page 14-17 BHD 18 + 3 page 18-21 BHD 17 + 3 page 18-21 BHDM 12 + 3 page 22-25 page 26-28 Boom Makina;

Difference in Technology. www.deltagroupcable.com

www.deltagroupcable.com www.deltagroupcable.com www.deltagroupcable.com www.deltagroupcable.com DELTA KABLO Türk kablo sektörünün en büyük

www.deltagroupcable.com www.deltagroupcable.com www.deltagroupcable.com www.deltagroupcable.com DELTA KABLO Türk kablo sektörünün en büyük

HİDROLİK VİNÇ KATALOĞU HYDRAULIC CRANE CATALOG

HİDROLİK VİNÇ KATALOĞU HYDRAULIC CRANE CATALOG sf 1 sf 2 KURUMSAL CORPORATE 1987 Yılından bugüne kadar 500 kapasiteden 200 ton a kadar çeşitli tiplerde kaldırma makinesi ve vinç üretimi ile faaliyetlerine

HİDROLİK VİNÇ KATALOĞU HYDRAULIC CRANE CATALOG sf 1 sf 2 KURUMSAL CORPORATE 1987 Yılından bugüne kadar 500 kapasiteden 200 ton a kadar çeşitli tiplerde kaldırma makinesi ve vinç üretimi ile faaliyetlerine

HİDROLİK VİNÇ KATALOĞU HYDRAULIC CRANE CATALOG

HİDROLİK VİNÇ KATALOĞU HYDRAULIC CRANE CATALOG sf 1 KURUMSAL 1987 Yılından bugüne kadar 500 kapasiteden 200 ton a kadar çeşitli tiplerde kaldırma makinesi ve vinç üretimi ile faaliyetlerine 10.000 m2 kapalı

HİDROLİK VİNÇ KATALOĞU HYDRAULIC CRANE CATALOG sf 1 KURUMSAL 1987 Yılından bugüne kadar 500 kapasiteden 200 ton a kadar çeşitli tiplerde kaldırma makinesi ve vinç üretimi ile faaliyetlerine 10.000 m2 kapalı

TURKISH ECONOMY PAST AND FUTURE Türkiye Ekonomisi. March 2013 DENİZ GÖKÇE

TURKISH ECONOMY PAST AND FUTURE Türkiye Ekonomisi March 2013 DENİZ GÖKÇE Dünya Borsa Kapitalizasyonu 2012 sonunda 54.57 trilyon dolar China s growing global economic influence (% global GDP) Çin in Dünya

TURKISH ECONOMY PAST AND FUTURE Türkiye Ekonomisi March 2013 DENİZ GÖKÇE Dünya Borsa Kapitalizasyonu 2012 sonunda 54.57 trilyon dolar China s growing global economic influence (% global GDP) Çin in Dünya

TÜRKÇE ÖRNEK-1 KARAALİ KÖYÜ NÜN MONOGRAFYASI ÖZET

TÜRKÇE ÖRNEK-1 KARAALİ KÖYÜ NÜN MONOGRAFYASI ÖZET Bu çalışmada, Karaali Köyü nün fiziki, beşeri, ekonomik coğrafya özellikleri ve coğrafi yapısının orada yaşayan insanlarla olan etkileşimi incelenmiştir.

TÜRKÇE ÖRNEK-1 KARAALİ KÖYÜ NÜN MONOGRAFYASI ÖZET Bu çalışmada, Karaali Köyü nün fiziki, beşeri, ekonomik coğrafya özellikleri ve coğrafi yapısının orada yaşayan insanlarla olan etkileşimi incelenmiştir.

PROFESYONEL HİJYEN EKİPMANLARI PROFESSIONAL HYGIENE PRODUCTS

PROFESYONEL HİJYEN EKİPMANLARI PROFESSIONAL HYGIENE PRODUCTS 2018 İçindekiler YENİ SIVI SABUN / KÖPÜK VERİCİ NEW SOAP / FOAM DISPENSER 3 1 YENİ SIVI SABUN / KÖPÜK VERİCİ 2 MAKSİ JUMBO TUVALET KAĞIT DİSPENSERİ

PROFESYONEL HİJYEN EKİPMANLARI PROFESSIONAL HYGIENE PRODUCTS 2018 İçindekiler YENİ SIVI SABUN / KÖPÜK VERİCİ NEW SOAP / FOAM DISPENSER 3 1 YENİ SIVI SABUN / KÖPÜK VERİCİ 2 MAKSİ JUMBO TUVALET KAĞIT DİSPENSERİ

TÜRK STANDARDI TURKISH STANDARD

TÜRK STANDARDI TURKISH STANDARD TS EN ISO 19011:2011 Ocak 2012 ICS 13.120.10;13.020.10 KALİTE VE ÇEVRE YÖNETİM SİSTEMLERİ TETKİK KILAVUZU Guidelines for quality and/or environmental management systems

TÜRK STANDARDI TURKISH STANDARD TS EN ISO 19011:2011 Ocak 2012 ICS 13.120.10;13.020.10 KALİTE VE ÇEVRE YÖNETİM SİSTEMLERİ TETKİK KILAVUZU Guidelines for quality and/or environmental management systems

Barometre 2014-II. Barometer

Barometre 2014-II Barometer YASED Barometre Anketi sorularının hazırlanmasındaki katkılarından ötürü Yöntem Research Consultancy Ltd e teşekkürlerimizi sunarız. We extend our sincere thanks to Yöntem Research

Barometre 2014-II Barometer YASED Barometre Anketi sorularının hazırlanmasındaki katkılarından ötürü Yöntem Research Consultancy Ltd e teşekkürlerimizi sunarız. We extend our sincere thanks to Yöntem Research

TURKISH NATURAL GAS MARKET

TURKISH NATURAL GAS MARKET REPORT 2017 All the information, tables and figures provided in this report are reserved and cannot be used without reference. REPUBLIC OF TURKEY ENERGY MARKET REGULATORY AUTHORITY

TURKISH NATURAL GAS MARKET REPORT 2017 All the information, tables and figures provided in this report are reserved and cannot be used without reference. REPUBLIC OF TURKEY ENERGY MARKET REGULATORY AUTHORITY

TURKISH NATURAL GAS MARKET REPORT This report is published within the scope of Official Statistics Programme.

TURKISH NATURAL GAS MARKET REPORT 2016 This report is published within the scope of Official Statistics Programme. All the information, tables and figures provided in this report are reserved and cannot

TURKISH NATURAL GAS MARKET REPORT 2016 This report is published within the scope of Official Statistics Programme. All the information, tables and figures provided in this report are reserved and cannot

Barometre 2014-I. Barometer

Barometre 2014-I Barometer YASED Barometre Anketi sorularının hazırlanmasındaki katkılarından ötürü Yöntem Research Consultancy Ltd e teşekkürlerimizi sunarız. We extend our sincere thanks to Yöntem Research

Barometre 2014-I Barometer YASED Barometre Anketi sorularının hazırlanmasındaki katkılarından ötürü Yöntem Research Consultancy Ltd e teşekkürlerimizi sunarız. We extend our sincere thanks to Yöntem Research

Argumentative Essay Nasıl Yazılır?

Argumentative Essay Nasıl Yazılır? Hüseyin Demirtaş Dersimiz: o Argumentative Essay o Format o Thesis o Örnek yazı Military service Outline Many countries have a professional army yet there is compulsory

Argumentative Essay Nasıl Yazılır? Hüseyin Demirtaş Dersimiz: o Argumentative Essay o Format o Thesis o Örnek yazı Military service Outline Many countries have a professional army yet there is compulsory

Yuratek olarak 2001 yılından beri medikal

www.yuratek.com Hakk m zda About Us Yuratek olarak 2001 yılından beri medikal sektöründe hizmet vermekteyiz. Yurtiçinde hastane, poliklinik ve özel muayenehaneler ile yurt dışında çeşitli firmalara hizmet

www.yuratek.com Hakk m zda About Us Yuratek olarak 2001 yılından beri medikal sektöründe hizmet vermekteyiz. Yurtiçinde hastane, poliklinik ve özel muayenehaneler ile yurt dışında çeşitli firmalara hizmet

ÜRÜN TEŞHİR STANDLARI ÜRETİMİ / DISPLAY DESIGN & PRODUCTION

ÜRÜN TEŞHİR STANDLARI ÜRETİMİ / DISPLAY DESIGN & PRODUCTION KURUMSAL Ürün teşhir standları üretimi konusunda 2008 yılında kurulan Relax Stand günden güne arttırdığı başarı grafiği,tasarım gücü ve teknolojik

ÜRÜN TEŞHİR STANDLARI ÜRETİMİ / DISPLAY DESIGN & PRODUCTION KURUMSAL Ürün teşhir standları üretimi konusunda 2008 yılında kurulan Relax Stand günden güne arttırdığı başarı grafiği,tasarım gücü ve teknolojik

OTOMOTİV SAN. TİC. LTD. ŞTİ. OTOMOTİV YEDEK PARÇA İMALATI AUTOMOTIVE SPARE PART MANUFACTURING

OTOMOTİV SAN. TİC. LTD. ŞTİ. www.ozaksen.com.tr OTOMOTİV YEDEK PARÇA İMALATI AUTOMOTIVE SPARE PART MANUFACTURING ÜRÜNLERİMİZ OUR PRODUCTS INTERCOOL BAĞLANTI BORULARI INTERCOOL CONNECTION PIPES... 4 YAĞ

OTOMOTİV SAN. TİC. LTD. ŞTİ. www.ozaksen.com.tr OTOMOTİV YEDEK PARÇA İMALATI AUTOMOTIVE SPARE PART MANUFACTURING ÜRÜNLERİMİZ OUR PRODUCTS INTERCOOL BAĞLANTI BORULARI INTERCOOL CONNECTION PIPES... 4 YAĞ

Borsa İstanbul A.Ş. Başkanlığına 34467 Emirgan / İSTANBUL

98/238 İÇSEL BİLGİLERE İLİŞKİN ÖZEL DURUM AÇIKLAMA FORMU Ortaklığın Ünvanı /Ortakların Adı Adresi : T.GARANTİ BANKASI A.Ş. : Levent Nispetiye Mah. Aytar Cad. No:2 34340 Beşiktaş/İSTANBUL Telefon ve Fax

98/238 İÇSEL BİLGİLERE İLİŞKİN ÖZEL DURUM AÇIKLAMA FORMU Ortaklığın Ünvanı /Ortakların Adı Adresi : T.GARANTİ BANKASI A.Ş. : Levent Nispetiye Mah. Aytar Cad. No:2 34340 Beşiktaş/İSTANBUL Telefon ve Fax

Profil Boru Demir Çelik

Profil Boru Demir Çelik Hakkımızda Fabrikamız; BORSAN PROFİL BORU DEMİR ÇELİK SAN. VE TİC. LTD. ŞTİ. 2007 Yılında Hatay'ın Payas İlçesinde 21.000 m2 açık, 10.000 m2 kapalı alan üzerine kurulmuştur. Bölgenin

Profil Boru Demir Çelik Hakkımızda Fabrikamız; BORSAN PROFİL BORU DEMİR ÇELİK SAN. VE TİC. LTD. ŞTİ. 2007 Yılında Hatay'ın Payas İlçesinde 21.000 m2 açık, 10.000 m2 kapalı alan üzerine kurulmuştur. Bölgenin

INDEX. Hakkımızda / About Us Fabrika / Factory Ürünler / Products

www.altarmarble.com INDEX Hakkımızda / About Us... 5 Fabrika / Factory... 6-9 Ürünler / Products Moon Cream... 12-13 Beach Cream... 14-15 Vanilla Ice... 16-17 Galaxy Silver... 18-19 Light Travertine...

www.altarmarble.com INDEX Hakkımızda / About Us... 5 Fabrika / Factory... 6-9 Ürünler / Products Moon Cream... 12-13 Beach Cream... 14-15 Vanilla Ice... 16-17 Galaxy Silver... 18-19 Light Travertine...

Küresel Rekabette İstanbul Sanayi Odası Meslek Komiteleri Sektör Stratejileri Projesi. Kok Kömürü ve Rafine Edilmiş Petrol Ürünleri İmalatı Sanayi

Küresel Rekabette İstanbul Sanayi Odası Meslek Komiteleri Sektör Stratejileri Projesi Kok Kömürü ve Rafine Edilmiş Petrol Ürünleri İmalatı Sanayi 1 2 Küresel Rekabette İstanbul Sanayi Odası Meslek Komiteleri

Küresel Rekabette İstanbul Sanayi Odası Meslek Komiteleri Sektör Stratejileri Projesi Kok Kömürü ve Rafine Edilmiş Petrol Ürünleri İmalatı Sanayi 1 2 Küresel Rekabette İstanbul Sanayi Odası Meslek Komiteleri

1 I S L U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 5 ) _ 3 0 K a s ı m

_ 3 0 K a s ı m") 1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 5 ) _ 3 0 K a s ı m 2 0 1 2 CEVAPLAR 1. Tekelci bir firmanın sabit bir ortalama ve marjinal maliyet ( = =$5) ile ürettiğini ve =53 şeklinde

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 5 ) _ 3 0 K a s ı m 2 0 1 2 CEVAPLAR 1. Tekelci bir firmanın sabit bir ortalama ve marjinal maliyet ( = =$5) ile ürettiğini ve =53 şeklinde

INSPIRE CAPACITY BUILDING IN TURKEY

Ministry of Environment and Urbanization General Directorate of Geographical Information Systems INSPIRE CAPACITY BUILDING IN TURKEY Section Manager Department of Geographical Information Agenda Background

Ministry of Environment and Urbanization General Directorate of Geographical Information Systems INSPIRE CAPACITY BUILDING IN TURKEY Section Manager Department of Geographical Information Agenda Background

Turizm Pazarlaması. Tourism Marketing

Turizm Pazarlaması Tourism Marketing 1980 li yılların başında dünya üzerinde seyahat eden turist sayısı 285 milyon ve toplam gelir 92 milyar dolar iken, 2000 yılında bu rakam, 698 milyona ulaşmış ve bu

Turizm Pazarlaması Tourism Marketing 1980 li yılların başında dünya üzerinde seyahat eden turist sayısı 285 milyon ve toplam gelir 92 milyar dolar iken, 2000 yılında bu rakam, 698 milyona ulaşmış ve bu

BİR BASKI GRUBU OLARAK TÜSİADTN TÜRKİYE'NİN AVRUPA BİRLİĞl'NE TAM ÜYELİK SÜRECİNDEKİ ROLÜNÜN YAZILI BASINDA SUNUMU

T.C. ANKARA ÜNİVERSİTESİ SOSYAL BİLİMLER ENSTİTÜSÜ HALKLA İLİŞKİLER VE TANITIM ANABİLİM DALI BİR BASKI GRUBU OLARAK TÜSİADTN TÜRKİYE'NİN AVRUPA BİRLİĞl'NE TAM ÜYELİK SÜRECİNDEKİ ROLÜNÜN YAZILI BASINDA

T.C. ANKARA ÜNİVERSİTESİ SOSYAL BİLİMLER ENSTİTÜSÜ HALKLA İLİŞKİLER VE TANITIM ANABİLİM DALI BİR BASKI GRUBU OLARAK TÜSİADTN TÜRKİYE'NİN AVRUPA BİRLİĞl'NE TAM ÜYELİK SÜRECİNDEKİ ROLÜNÜN YAZILI BASINDA

Possible Effects of a Hike in BRENT Prices on Turkey's Energy Bills and Current Account Deficit

Possible Effects of a Hike in BRENT Prices on Turkey's Energy Bills and Current Account Deficit Turbulence in Mosul is threatening global markets pushing up oil prices up due to worries of cuts in supply.

Possible Effects of a Hike in BRENT Prices on Turkey's Energy Bills and Current Account Deficit Turbulence in Mosul is threatening global markets pushing up oil prices up due to worries of cuts in supply.

Association of Turkish Furniture Manufacturers MOSDER Chairman Ramazan

Türkiye Mobilya Sanayicileri Derneği MOSDER Yönetim Kurulu Başkanı Ramazan DAVULCUOĞLU Association of Turkish Furniture Manufacturers MOSDER Chairman Ramazan DAVULCUOĞLU 15 Haziran 2012, İzmir GÜCÜMÜZ

Türkiye Mobilya Sanayicileri Derneği MOSDER Yönetim Kurulu Başkanı Ramazan DAVULCUOĞLU Association of Turkish Furniture Manufacturers MOSDER Chairman Ramazan DAVULCUOĞLU 15 Haziran 2012, İzmir GÜCÜMÜZ

Dünya devinin gücünü hissedin

Türkiye Distribütörü Feel the power of world giant Dünya devinin gücünü hissedin Yıllık üretim 110.000 adet Kapalı üretim alanı 7.000 m² 10msn hız İleri teknoloji Çevreci Annual capacity 110.000 pcs Building

Türkiye Distribütörü Feel the power of world giant Dünya devinin gücünü hissedin Yıllık üretim 110.000 adet Kapalı üretim alanı 7.000 m² 10msn hız İleri teknoloji Çevreci Annual capacity 110.000 pcs Building

UFRS YE TABİ OLACAK KOBİ LERDE BAĞIMSIZ DIŞ DENETİMİN FAALİYET SONUÇLARI ÜZERİNE OLASI ETKİLERİ

T.C. Hitit Üniversitesi Sosyal Bilimler Enstitüsü İşletme Anabilim Dalı UFRS YE TABİ OLACAK KOBİ LERDE BAĞIMSIZ DIŞ DENETİMİN FAALİYET SONUÇLARI ÜZERİNE OLASI ETKİLERİ Elif KURTCU Yüksek Lisans Tezi Çorum

T.C. Hitit Üniversitesi Sosyal Bilimler Enstitüsü İşletme Anabilim Dalı UFRS YE TABİ OLACAK KOBİ LERDE BAĞIMSIZ DIŞ DENETİMİN FAALİYET SONUÇLARI ÜZERİNE OLASI ETKİLERİ Elif KURTCU Yüksek Lisans Tezi Çorum

İTKİB GENEL SEKRETERLİĞİ

I TKI B-Kayıt belgesi -ÖNEMLI DUYURU Bilindiği üzere, 2010/1 sayılı İthalatta Gözetim Uygulanmasına İlişkin Tebliğ kapsamında bahse konu tebliğin ekinde belirtilen gümrük tarife istatistik pozisyonu altında

I TKI B-Kayıt belgesi -ÖNEMLI DUYURU Bilindiği üzere, 2010/1 sayılı İthalatta Gözetim Uygulanmasına İlişkin Tebliğ kapsamında bahse konu tebliğin ekinde belirtilen gümrük tarife istatistik pozisyonu altında

MİSYONUMUZ OUR MISSION VİZYONUMUZ OUR VISION

www.adaset.com www.adaset.com MİSYONUMUZ Şirketimizin sürekli gelişen organizasyon yapısı içinde daha kaliteli ürün ve hizmet vermesini sağlamak ve modern yönetim anlayışıyla yeniliklere imza atan, global

www.adaset.com www.adaset.com MİSYONUMUZ Şirketimizin sürekli gelişen organizasyon yapısı içinde daha kaliteli ürün ve hizmet vermesini sağlamak ve modern yönetim anlayışıyla yeniliklere imza atan, global

TKMP BİLEŞENLER / COMPONENTS

MASS VALUATION ACTIVITIES CONDUCTED BY GENERAL DIRECTORATE OF LAND REGISTRY AND CADASTRE TAPU VE KADASTRO GENEL MÜDÜRLÜĞÜ TARAFINDAN YÜRÜTÜLEN TOPLU DEĞERLEME ÇALIŞMALARI TKMP BİLEŞENLER / COMPONENTS Land

MASS VALUATION ACTIVITIES CONDUCTED BY GENERAL DIRECTORATE OF LAND REGISTRY AND CADASTRE TAPU VE KADASTRO GENEL MÜDÜRLÜĞÜ TARAFINDAN YÜRÜTÜLEN TOPLU DEĞERLEME ÇALIŞMALARI TKMP BİLEŞENLER / COMPONENTS Land

Technical Assistance for Increasing Primary School Attendance Rate of Children

This Project is co-financed by the European Union and the Republic of Turkey. Technical Assistance for Increasing Primary School Attendance Rate of Children This project is co-financed by the European

This Project is co-financed by the European Union and the Republic of Turkey. Technical Assistance for Increasing Primary School Attendance Rate of Children This project is co-financed by the European

SEMPOZYUMU KASIM 2015 ANTALYA. Dr. Yakup UMUCU

SEMPOZYUMU 26-27 KASIM 2015 ANTALYA Dr. Yakup UMUCU - ISBN : 978-605-01-0792-0 Tel : Kamel Audio Kaset- : (0 212) 4773580 (pbx) : NKARA Tel : (0.312) 425 10 80 Fax: (0.312) 417 52 90 : www.maden.org.tr

SEMPOZYUMU 26-27 KASIM 2015 ANTALYA Dr. Yakup UMUCU - ISBN : 978-605-01-0792-0 Tel : Kamel Audio Kaset- : (0 212) 4773580 (pbx) : NKARA Tel : (0.312) 425 10 80 Fax: (0.312) 417 52 90 : www.maden.org.tr

ÇEVRESEL TEST HİZMETLERİ 2.ENVIRONMENTAL TESTS

ÇEVRESEL TEST HİZMETLERİ 2.ENVIRONMENTAL TESTS Çevresel testler askeri ve sivil amaçlı kullanılan alt sistem ve sistemlerin ömür devirleri boyunca karşı karşıya kalabilecekleri doğal çevre şartlarına dirençlerini

ÇEVRESEL TEST HİZMETLERİ 2.ENVIRONMENTAL TESTS Çevresel testler askeri ve sivil amaçlı kullanılan alt sistem ve sistemlerin ömür devirleri boyunca karşı karşıya kalabilecekleri doğal çevre şartlarına dirençlerini

Ürün Kataloğu Product catalogue

www.elcalu.com.tr Ürün Kataloğu Product catalogue www.elcalu.com.tr HAKKIMIZDA ABOUT US ELC ALÜMİNYUM SAN. TİC. A.Ş. 40 yıllık metal üretim ve işleme tecrübesini alüminyum mamul üretimine aktarmak üzere,

www.elcalu.com.tr Ürün Kataloğu Product catalogue www.elcalu.com.tr HAKKIMIZDA ABOUT US ELC ALÜMİNYUM SAN. TİC. A.Ş. 40 yıllık metal üretim ve işleme tecrübesini alüminyum mamul üretimine aktarmak üzere,

KALİTE, GÜVEN QUALITY, CONFIDENCE STARTER BATTERY PRODUCT CATALOG

KALİTE, GÜVEN QUALITY, CONFIDENCE STARTER BATTERY PRODUCT CATALOG CORPORATE Volt ba ery industry and trade ıncorporate company was founded in 1989 in Izmir in order to produce accumulators and materials

KALİTE, GÜVEN QUALITY, CONFIDENCE STARTER BATTERY PRODUCT CATALOG CORPORATE Volt ba ery industry and trade ıncorporate company was founded in 1989 in Izmir in order to produce accumulators and materials

Prof. Dr. N. Lerzan ÖZKALE

ERASMUS + YÜKSEKÖĞRETİM YIL SONU DEĞERLENDİRME TOPLANTISI Akdeniz Üniversitesi, Antalya AKADEMİK TANINMA Prof. Dr. N. Lerzan ÖZKALE İstanbul Teknik Üniversitesi ve Kadir Has Üniversitesi 21 Aralık 2017

ERASMUS + YÜKSEKÖĞRETİM YIL SONU DEĞERLENDİRME TOPLANTISI Akdeniz Üniversitesi, Antalya AKADEMİK TANINMA Prof. Dr. N. Lerzan ÖZKALE İstanbul Teknik Üniversitesi ve Kadir Has Üniversitesi 21 Aralık 2017

ANKARA DEMİR VE DEMİR DIŞI METALLER İHRACATÇILARI BİRLİĞİ. SİRKÜLER (D-2018) Sayın Üyemiz,

Sayın Üyemiz,") ANKARA DEMİR VE DEMİR DIŞI METALLER İHRACATÇILARI BİRLİĞİ Sayı: 21704200-TİM.OAİB.11.2018/20012-20103 Ankara, 04/07/2018 Konu: AB Koruma Önlemi Soruşturması SİRKÜLER (D-2018) Sayın Üyemiz, Avrupa Birliği

ANKARA DEMİR VE DEMİR DIŞI METALLER İHRACATÇILARI BİRLİĞİ Sayı: 21704200-TİM.OAİB.11.2018/20012-20103 Ankara, 04/07/2018 Konu: AB Koruma Önlemi Soruşturması SİRKÜLER (D-2018) Sayın Üyemiz, Avrupa Birliği

FVAÖK yıllık bazda %129 artmış ve FVAÖK marjı da 9A09 da %12 olmuştur. Bu artış ARGE teşvikleri ve maliyet düşürücü önlemlerden kaynaklanmaktadır.

9A09 (mntl) Satışlar FVAÖK Net Kar Açıklanan 160 19 23 GY tahmini 159 21 25 Netaş 9A09 finansal sonuçlarında 23mn TL net kar açıkladı, ki bu da bizim beklentimiz olan 25mn TL net karın biraz altındadır.

9A09 (mntl) Satışlar FVAÖK Net Kar Açıklanan 160 19 23 GY tahmini 159 21 25 Netaş 9A09 finansal sonuçlarında 23mn TL net kar açıkladı, ki bu da bizim beklentimiz olan 25mn TL net karın biraz altındadır.

2012 YILI. Faaliyet Raporu. I. Uluslararası Enetelektüel Sermayenin. Ölçülmesi ve Roparlanması. Sempozyumu

I. Uluslararası Enetelektüel Sermayenin Ölçülmesi ve Roparlanması Sempozyumu 2012 396 I. Uluslararası Entelektüel Sermayenin Ölçülmesi ve Raporlanması Sempozyumu İstanbul Kalkınma Ajansı (ISTKA) nın Kar

I. Uluslararası Enetelektüel Sermayenin Ölçülmesi ve Roparlanması Sempozyumu 2012 396 I. Uluslararası Entelektüel Sermayenin Ölçülmesi ve Raporlanması Sempozyumu İstanbul Kalkınma Ajansı (ISTKA) nın Kar

TECHNICAL WIND RESOURCE CAPACITY of TURKEY (1/2)

") TECHNICAL WIND RESOURCE CAPACITY of TURKEY (1/2) TECHNICAL WIND RESOURCE CAPACITY of TURKEY (2/2) «REPA» WIND ATLAS prepared by General Directorate of Renewable Energy (former EIE) indicates wind resource

TECHNICAL WIND RESOURCE CAPACITY of TURKEY (1/2) TECHNICAL WIND RESOURCE CAPACITY of TURKEY (2/2) «REPA» WIND ATLAS prepared by General Directorate of Renewable Energy (former EIE) indicates wind resource

(THE SITUATION OF VALUE ADDED TAX IN THE WORLD IN THE LIGHT OF OECD DATA)

") H OECD VERİLERİ IŞIĞINDA DÜNYADA KATMA DEĞER VERGİSİNİN DURUMU * (THE SITUATION OF VALUE ADDED TAX IN THE WORLD IN THE LIGHT OF OECD DATA) Yusuf ARTAR (Vergi Müfettişi/Tax Inspector) ÖZ Dünyada ilk olarak

H OECD VERİLERİ IŞIĞINDA DÜNYADA KATMA DEĞER VERGİSİNİN DURUMU * (THE SITUATION OF VALUE ADDED TAX IN THE WORLD IN THE LIGHT OF OECD DATA) Yusuf ARTAR (Vergi Müfettişi/Tax Inspector) ÖZ Dünyada ilk olarak

YARASA VE ÇİFTLİK GÜBRESİNİN BAZI TOPRAK ÖZELLİKLERİ ve BUĞDAY BİTKİSİNİN VERİM PARAMETRELERİ ÜZERİNE ETKİSİ

ATATÜRK ÜNİVERSİTESİ FEN BİLİMLERİ ENSTİTÜSÜ DOKTORA TEZİ YARASA VE ÇİFTLİK GÜBRESİNİN BAZI TOPRAK ÖZELLİKLERİ ve BUĞDAY BİTKİSİNİN VERİM PARAMETRELERİ ÜZERİNE ETKİSİ TARIMSAL YAPILAR VE SULAMA ANABİLİM

ATATÜRK ÜNİVERSİTESİ FEN BİLİMLERİ ENSTİTÜSÜ DOKTORA TEZİ YARASA VE ÇİFTLİK GÜBRESİNİN BAZI TOPRAK ÖZELLİKLERİ ve BUĞDAY BİTKİSİNİN VERİM PARAMETRELERİ ÜZERİNE ETKİSİ TARIMSAL YAPILAR VE SULAMA ANABİLİM